1) Visa, Mastercard vs digital wallets 2) Where is the big BNPL play heading?

Welcome to my newsletter! Each week two hand-picked topics from the world of fintech, payments and banking with behind-the-scenes analysis!

1) Visa, Mastercard vs digital wallets

It was a matter of time. Mastercard is going after Visa, and both are after digital wallets. Can the schemes really replace digital wallets and how do they want to pull it off? Let’s take a look.

On May 15th, 2024, Visa announced Visa Flexible Credential (VFC). And a few days ago, Mastercard announced Mastercard One Credential (MOC).

The idea behind both is the same: in a world with increasing digital wallet dominance both schemes want to re-invent their card offering and re-position themselves directly against digital wallets.

Here is the strategy:

- Visa and Mastercard are reversing the existing card logic on its head by consolidating multiple payment methods into one card.

- This marks a transition from one card with one payment method to one card with many funding sources.

- Instead of having to use one credit or debit card you can now have different funding options (debit, credit, BNPL, rewards points) connected to any card and be able to switch between them via the app.

The logic is exactly the same with the one behind digital wallets and the intention is clear. The big schemes want a slice of the pie.

Here is how this will work in practice:

End consumers will set, online or in-app (from participating issuers), their spending preferences against their preferred funding sources. For example, I might set BNPL as my default for on-line shopping or larger purchases, whereas at the same time I might choose to charge travel expenses via credit and supermarket via my account.

Implications:

1. Cards are now directly competing with digital wallets.

2. It’s an ecosystem play. The broader it gets the more the added value to the customers. Which is why both schemes made sure to announce a few big partner names at launch. Visa with Liv digital bank, Affirm and Japan’s Sumitomo Mitsui Financial Group wheres Mastercard with Episode Six, Marqueta, Bendigo and Adelaide Bank Group, Galileo Financial Technologies, i2c, Lithic, and Wio Bank.

3. Higher degree of flexibility, personalization and targeted focus for banks and fintechs.

4. Expect to see additional funding sources to be added gradually (i.e. crypto).

5. The same way Visa pushed Mastercard to follow suit, I think it’s a matter of time before American Express and Discover announce similar initiatives.

6. For issuers it might be an opportunity to connect ecosystems and bring different capabilities under the same roof.

7. Can transform the SMB and SME landscape by acting as a bridge between business and consumer accounts (potential to switch with the same credential).

One thing is certain: for both networks this is a long-term, strategic game that aims at cementing their positioning as a wider infrastructure enabler. Visa calls it in their strategy a network of networks and it’s exactly that.

Opinions: Panagiotis Kriaris, Graphic sources: Visa, Mastercard

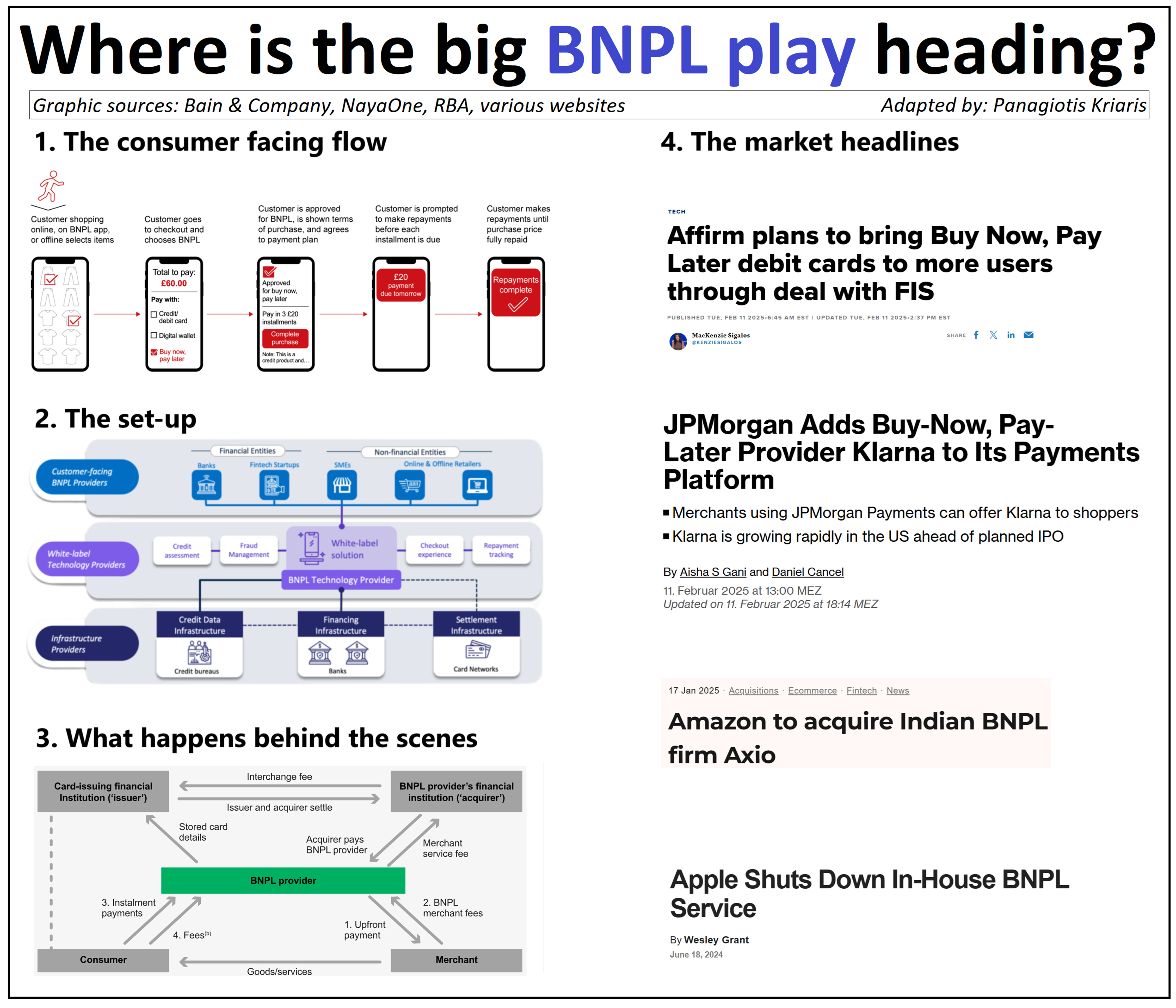

2) Where is the big BNPL play heading?

For the big players BNPL is an indispensable play. But that’s not a surprise. The question is why more and more choose to pursue this outside of their core, despite their size and scale. Let’s take a look.

Just a few days ago FIS announced a partnership with BNPL giant Affirm via which they will introduce instalments into traditional debit cards:

- To do so FIS will directly embed Affirm’s offering (BNPL is anyhow an embedded finance play) into their payment processing set-up.

- The embedded integration model brings the huge benefit of bypassing individual direct integrations, providing direct access to Affirm’s 335,000 strong merchant network

- Banks can also offer instalments through their debit card programs

Almost at the same time JPMorgan announced a partnership with Klarna:

- Similarly JPMorgan (Payments) will directly integrate Klarna into its existing merchant services infrastructure (Commerce Solutions).

- JPMorgan Payments is the world's largest merchant acquirer with $2tn+ in payment volumes, whereas Klarna is preparing for a $15bn IPO, one of largest this year.

In January this year, Amazon agreed to pay $160mn to acquire Indian BNPL player Axio after holding a stake for 6 years:

- With Axio Amazon doubled down on the growth and potential of the Indian market, getting access to more than 10mn customers and a loan book of $260mn.

Last year Apple exited its own BNPL model, only to intensify focus on the model by partnering up with (different) partners across geographies:

- The model proved to complex to keep in house even for a player with the size and resources of Apple.

- Apple will still retain control without having to directly manage the business.

What all the above tell us? A few key things:

1. BNPL has become much more than a single, stand-alone offering. It has moved up the value chain with holistic payment strategies that cut across modern shopping habits: marketplaces, digital wallets, credit and debit cards.

2. BNPL might be a simple concept, but the set-up behind (product, technology, underwriting, collections) can be quite complex. Building it in house is not easy, even for big players. Flexibility, scale potential, regional expertise and speed-to-market are some of the main reasons.

3. Regulatory scrutiny for BNPL is tightening around the globe, affecting both costs and reporting. Managing these is not attractive.

4. BNPL is, in effect, unsecured lending with strict capital and risk provisioning requirements. Balance-sheet appetite is not there for most players who prefer either a third party or a specialized vehicle that works (Axio example).

BNPL will continue to make headlines (and profits) for time to come.

Opinions: my own, Graphic sources: Bain & Company, NayaOne, RBA, various websites