1) The corporate cards' opportunity 2) Banks' BNPL opportunity

Welcome to my newsletter! Each week two hand-picked topics from the world of fintech, payments and banking with behind-the-scenes analysis!

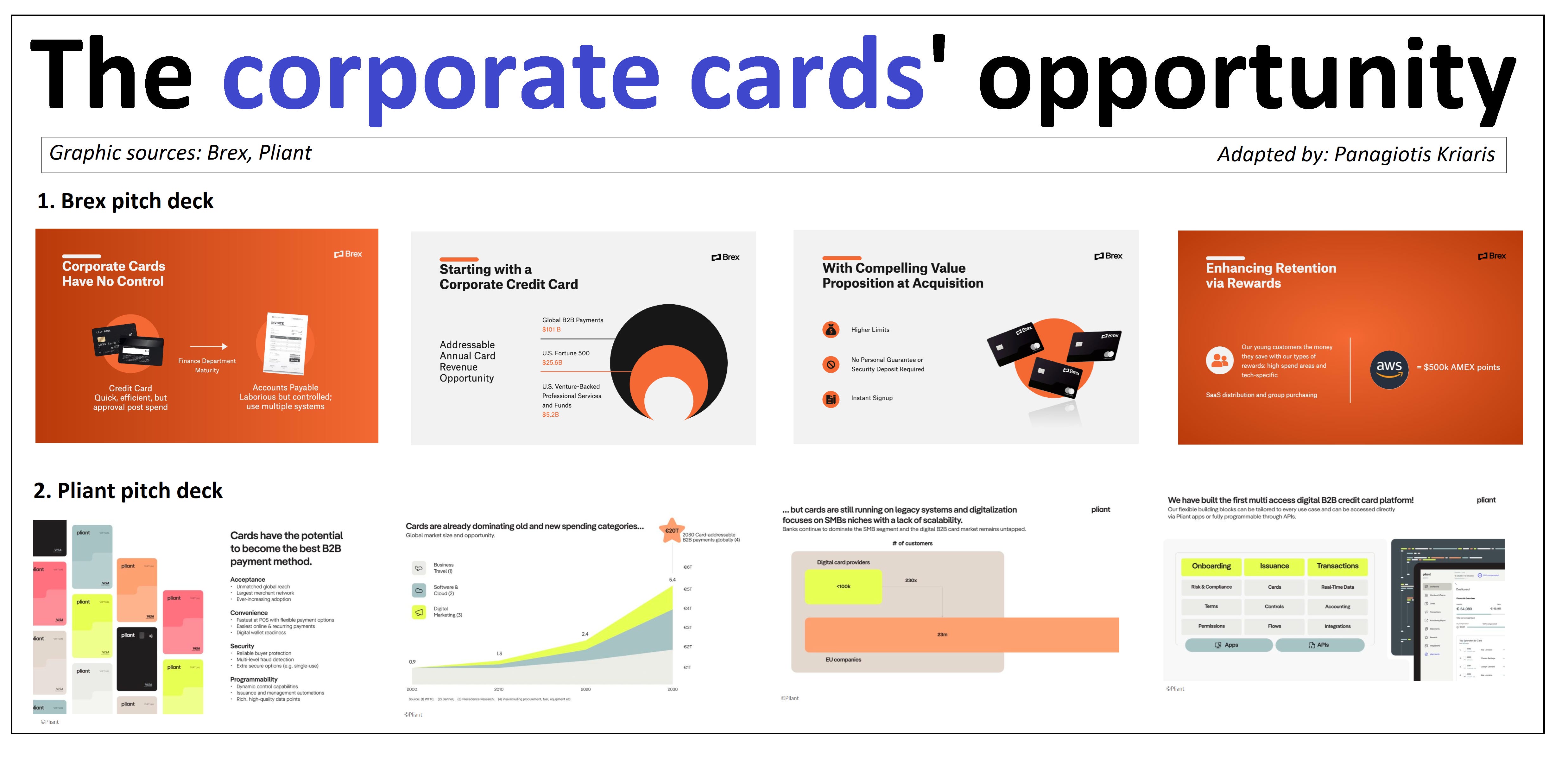

1) The corporate cards' opportunity

B2B payments are one of the largest untapped opportunities in finance, and corporate cards are one of the best examples of the disruption potential. Let’s take a look.

Traditional banks have long dominated the corporate card market, however mostly with subpar offerings:

- Extensive paperwork

- Lengthy approval processes

- Complex terms

- Strict spending limits

- Poor UX

- Lack of flexibility

- No real-time capabilities (post spend approval)

A number of fintechs (Brex, Pliant, Ramp and Bill are good examples - there are more) have spotted the opportunity and whereas there is no one-size-fits-all recipe, here’s my summary of methods they have used to be successful:

1. Focus on the customer experience (simplify the UX, solve for problems).

2. Use technology to build flexibility and allow for personalization (i.e. customized spending categories).

3. Fast and efficient onboarding.

4. Streamline expense management. Example functionalities include automated reconciliation tools, flexible payment terms, real-time expense tracking, instant virtual cards, etc.

4. Optimize risk and fraud management as a crucial capability. Managing credit risk is a pillar of their their competitive edge: do it efficiently and it allows to beat the banks in their own game by offering higher credit lines, while at the same time minimizing defaults.

5. Focus on verticals with high-monetization potential and expand from there. Technology companies or the travel sector are good examples. Brex’s partnership with Navan is a characteristic example: it allows automated travel payment reconciliation on bookings made through Navan via a direct Brex integration into Navan’s travel management software.

6. Embed into offerings from partners in other parts of the value chain. Pliant has integrated with Candis, an invoice management software provider, and Circula, a travel expense and employee benefits software provider.

7. Play the software game. Which means that corporate cards become just one of many pillars of a wider ecosystem play that focuses on financial management for enterprise customers. Software+cards+payments.

8. Use creative ways to fund growth beyond the funding series. For example, securitization of client-card payments can be a useful tool, but it is subject to size constraints, investor appetite and macro developments.

B2Bpayments are undergoing their greatest transformation so far. Corporate cards are just one aspect of this huge revenue pool and indicative of the opportunity.

Opinions: my own, Graphic sources: Brex and Pliant pitch decks

2) Banks' BNPL opportunity

It doesn’t make any sense. Banks have lost the BNPL opportunity in a business that lies at the core of what they do. Let’s take a look.

BNPL consumer demand is stronger than ever (Worldplay Global Payments Report 2024): Global BNPL transaction values will hit $452 bn in 2027 vs $316 bn in 2023.

And yet they represent a fraction of the market (ecommerce 5%, POS 2%). BNPL is still in its infancy.

Which is why everyone has been jumping to the BNPL wagon: fintech providers (i.e. Affirm, Afterpay, Klarna), BigTechs (i.e. Apple, Amazon, Google), payment players (i.e. Visa, Mastercard, PayPal), marketplaces and brands.

However, there is a double oxymoron:

1) The BNPL winners are increasingly players for whom BNPL is not the primary business model

2) Banks have mostly been at the bottom of the adoption curve, in spite of BNPL being a credit offering

Why?

— Slow reflexes

— Outdated, inflexible infrastructure

— BNPL perceived as competition

— Lack of an agile, #innovation-first approach

What banks do not realize is that BNPL:

— Can add value to their existing product lines and widen customer relationships

— Is a connection to customer segments they can otherwise not approach (i.e. millennials)

— Is a new growth source with low customer acquisition cost

— Opens the door to other strategic plays: embedded finance, in-app shopping, digital wallets, marketplace banking

— Is a must-have to compete in payments

Plus, banks are well positioned:

1. As licensed entities can navigate the regulatory push

2. Can build on scale and trust

Depending on size, resources and strategy there are a few ways to do it:

— Build own offering: e.g., Santander has positioned BNPL at the core of its strategy by launching in 2022 its own BNPL offering (Zinia)

— Outsource to a provider and white label following the BaaS model: e.g. Barclays became one of the first major banks in America to offer POS financing via platform player Amount in 2021

The former model requires advanced technological and risk underwriting capabilities as well as a sophisticated check-out flow, whereas the latter piggybacks on the providers’ expertise, usually on a modular basis.

Important things to consider:

— BNPL is not just a financing option, but a holistic check-out approach in its own right. Addressing the end2end customer journey is critical

— Compliance, fraud and dunning can be a make-or-break factors

— The BaaS model offers opportunities on different levels of the value chain. E.g. smaller banks with no expertise can act as a mere balance-sheet provider

— There are synergies on multiple fronts: merchant acquiring, card issuing, cash management, retail banking are examples

BNPL is a strategic play for banks. They can either build on their strengths or can sit and watch their core business being eaten away.

Opinions: my own, Graphic source: Publicis Sapient