1) The AI-native Bank 2) The evolution of Payments 3) From AI to Multi-Agent Systems 4) ChatGPT guide

Welcome to my newsletter! Each week a few hand-picked topics from the world of fintech, payments and banking with behind-the-scenes analysis! Plus if you are at Money20/20 this week, let's meet up!

1) The AI-native Bank

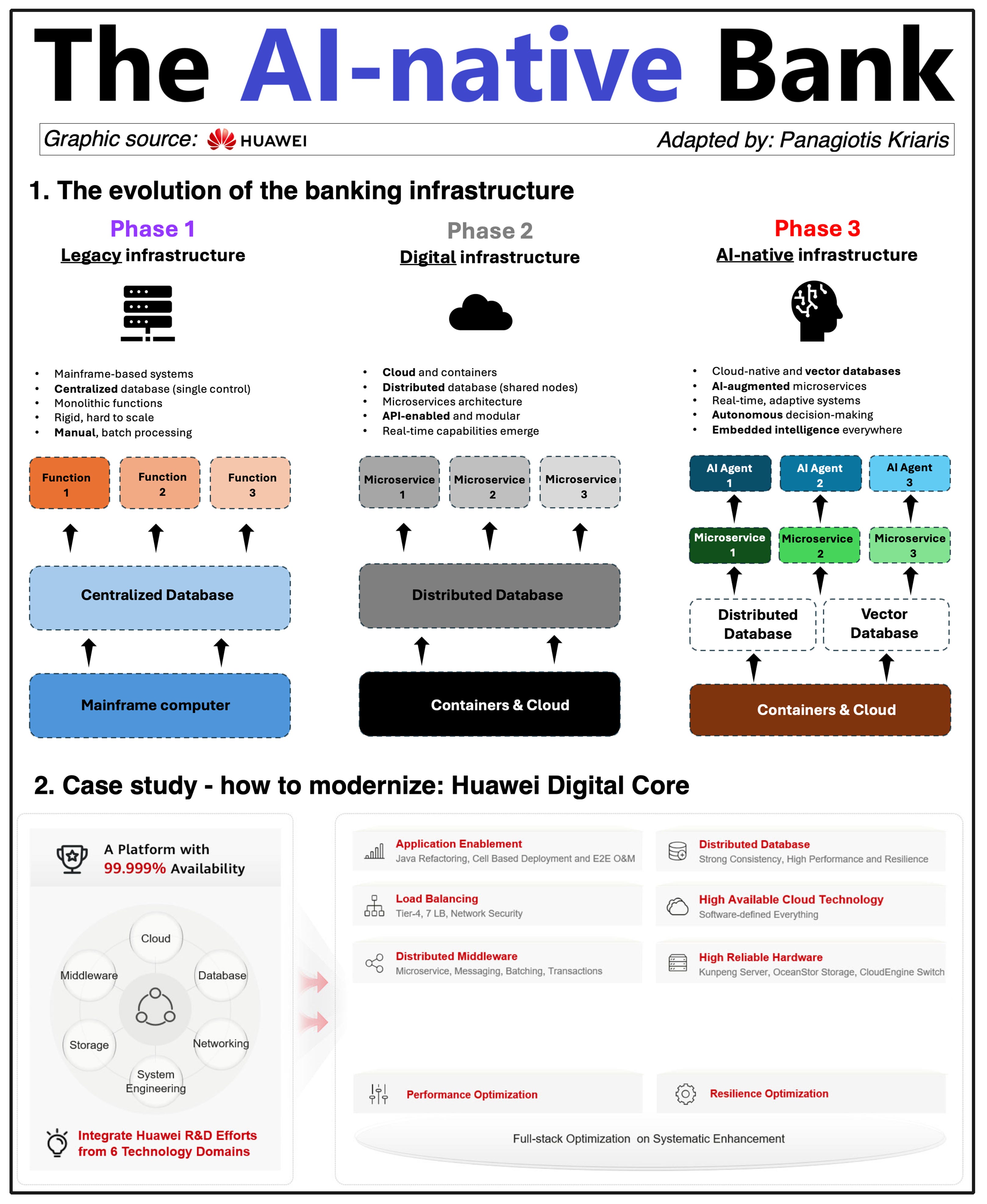

Every bank must become AI-native. Most banks understand the imperative, yet rigid, decades-old infrastructure stands in the way. Are there practical strategies to bridge the gap?

The evolution of banking infrastructure explains why some banks move faster than others – and what it takes to compete in an AI-driven world.

Phase 1: Legacy

Banks ran on monolithic mainframes and a single database, processing transactions in nightly batches. This setup was relatively reliable but inflexible - every change required months of coding, testing, and downtime.

Phase 2: Digital

Banks deploy services as independent microservices in the cloud, with distributed data stores for instant access. APIs connect partners and internal systems, enabling real-time payments, rapid feature releases, and continuous updates.

Phase 3: AI-Native

AI agents will sit atop this digital core to make instant credit decisions, detect fraud as it happens, and tailor every interaction. Models will learn from live data, automating workflows and delivering hyper-personalized banking at scale.

Here are the core outcomes of phase 3 and their technical enablers.

1. Instant transactions: enabled by a data streaming platform that captures and routes events as they happen.

2. Five-nines reliability: 99.999% uptime - enabled by active-active database replication and automated failover across multiple data centers.

3. Mass personalization: enabled by a “vector” database that organizes unstructured text and interaction data.

4. Rapid product delivery: enabled by packaging functionality into lightweight containers managed by an orchestration system.

5. Seamless partner integration: enabled by a centralized API gateway that governs, secures, and monitors all external connections.

6. Continuous AI improvement: enabled by an MLOps platform that automates the full AI lifecycle - training, testing, deployment, and monitoring -ensuring models stay accurate as new data flows in.

7. Autonomous Decision-Making: enabled by AI agents built on microservices that execute pre-trained models in real time.

And now comes the hardest part – is there actually a model that helps banks modernize their legacy systems in a balanced way?

Huawei has one of the best approaches I have seen on the market: it’s called Huawei Digital CORE Solution and helps upgrade legacy to an agile, resilient, and open distributed platform. To do so they have integrated Huawei’s R&D results - Huawei is one of the world's largest patent holders - from 6 key domains:

1. Cloud

2. Middleware

3. Databases

4. Storage

5. Networking

6. System Engineering

Banks will jump into the AI wagon one way or the other. But 3 factors will decide who gets to be successful: 1) the timing 2) the approach 3) the partner.

Opinions: Panagiotis Kriaris, graphic source: Huawei

2) The evolution of Payments

Payments have evolved from paper and plastic to APIs and orchestration - giving rise to a new breed of players that simplify the complexity and connect the dots behind the scenes. Here's how we got here.

𝟭. 𝗜𝗻 𝘁𝗵𝗲 𝗽𝗿𝗲-𝟭𝟵𝟵𝟬𝘀 𝗲𝗿𝗮, banks owned the entire payments value chain -acquiring, processing, settlement. Merchant onboarding was complex, and domestic clearing systems ruled.

𝟮. 𝗧𝗵𝗲 𝗿𝗶𝘀𝗲 𝗼𝗳 𝗲-𝗰𝗼𝗺𝗺𝗲𝗿𝗰𝗲 in the late 1990s changed everything. Players like PayPal and Authorize made online payments possible, while banks began exiting the acquiring space or partnering with processors to keep up with demand.

𝟯. 𝗕𝗲𝘁𝘄𝗲𝗲𝗻 𝟮𝟬𝟬𝟬 𝗮𝗻𝗱 𝟮𝟬𝟭𝟬, specialized gateways and regional wallets began to scale, offering merchants greater flexibility and control. The launch of SEPA in Europe marked a push toward payment harmonization, while non-bank players started building infrastructure that bypassed traditional acquiring models altogether.

𝟰. 𝗧𝗵𝗲 𝘀𝗵𝗶𝗳𝘁 𝘁𝗼 𝗔𝗣𝗜-𝗱𝗿𝗶𝘃𝗲𝗻 𝗶𝗻𝗳𝗿𝗮𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲 transformed payments from siloed systems into modular, developer-friendly tools. Merchant onboarding became faster, integrations simpler, and innovation more scalable. Open Banking regulations enabled direct access to bank data, while new credit models redefined consumer behavior. Payments evolved into a flexible, programmable layer of the digital economy.

𝟱. 𝗧𝗼𝗱𝗮𝘆, we’re in the age of seamless integration. Payments are embedded in everything - from ride-hailing apps to SuperApps. Real-time rails like SEPA Instant, UPI and PIX are live. CBDCs are in pilot.

However, as payment ecosystems grow more fragmented - with new methods, regional schemes, compliance layers, and fraud risks -complexity has become a major bottleneck for merchants, fintechs, and even banks. Integrating multiple providers, maintaining uptime across systems, and ensuring regulatory compliance isn't just costly - it's unsustainable without the right foundation.

This is where a new breed of infrastructure players like 𝗔𝗸𝘂𝗿𝗮𝘁𝗲𝗰𝗼 fit in - offering the tools to simplify complexity and still retain control.

• 𝗪𝗵𝗶𝘁𝗲-𝗹𝗮𝗯𝗲𝗹 𝗽𝗮𝘆𝗺𝗲𝗻𝘁 𝗴𝗮𝘁𝗲𝘄𝗮𝘆𝘀 let banks, PSPs, and fintechs launch their own branded platforms fast - without building from scratch.

• 𝗣𝗮𝘆𝗺𝗲𝗻𝘁 𝗼𝗿𝗰𝗵𝗲𝘀𝘁𝗿𝗮𝘁𝗶𝗼𝗻 enables merchants to route transactions dynamically across multiple acquirers, reducing costs and failed payments while improving UX.

• 𝗕𝗮𝗻𝗸𝘀 can embed API-driven acquiring services into their offerings without the burden of a full-scale tech overhaul.

In a world where growth brings fragmentation, the real challenge isn’t enabling payments - it’s managing them. The advantage will lie with infrastructure that can unify complexity, adapt in real time, and scale across borders without adding friction.

Opinions: Panagiotis Kriaris, Graphic source: Akurateco Payment Hub

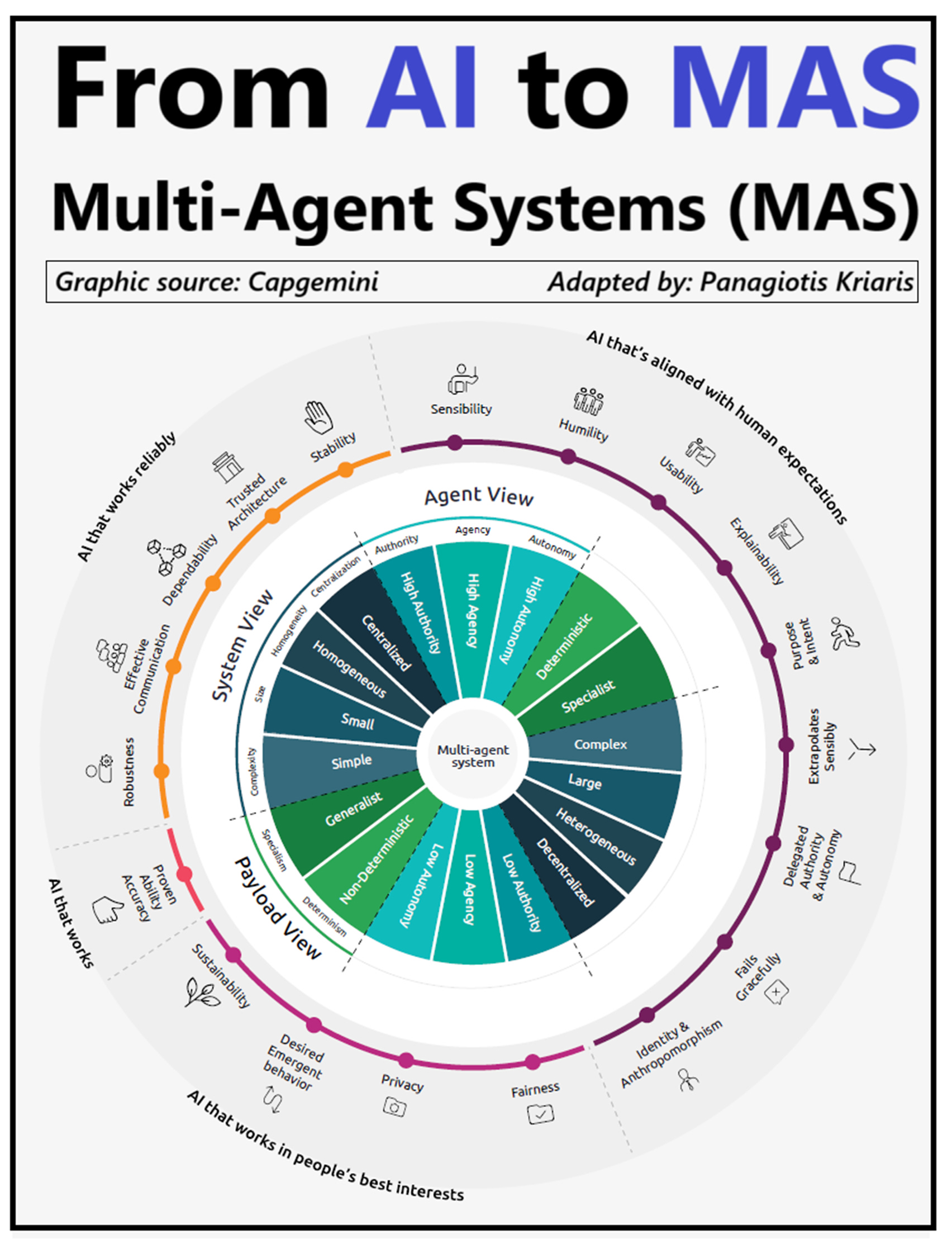

3) From AI to Multi-Agent Systems (MAS)

Everyone is talking about agentic AI and yet the next frontier is already in the making: Multi-Agent Systems (MAS).

AI didn’t arrive all at once – although in many cases it might seem it did. It evolved in distinct phases, each unlocking new capabilities and changing how work gets done:

𝟭. 𝗧𝗿𝗮𝗱𝗶𝘁𝗶𝗼𝗻𝗮𝗹 𝗔𝗜 (𝗣𝗿𝗲𝗱𝗶𝗰𝘁𝗶𝘃𝗲 𝗔𝗜):

- Systems powering rule-based models and statistical inference to detect fraud, recommend investments, and process documents - all in response to human prompts.

- Financial Services (FS) example: Credit scoring models and fraud detection engines improved efficiency, but remained passive tools waiting on human input.

𝟮. 𝗚𝗲𝗻𝗲𝗿𝗮𝘁𝗶𝘃𝗲 𝗔𝗜 (𝗚𝗲𝗻𝗔𝗜):

- LLMs and foundation models that brought language fluency and contextual understanding. These systems can create, explain, and summarize - moving from data crunching to content generation.

- FS example: Chatbots that summarize regulatory filings, generate client reports, or support advisors with contextual investment narratives.

𝟯. 𝗔𝗴𝗲𝗻𝘁𝗶𝗰 𝗔𝗜:

- Systems that can interpret goals, plan actions, and operate independently within constraints. These agents shift the human role from executing tasks to defining intent.

- FS example: AI agents that autonomously rebalance portfolios based on client preferences and market movements - no human intervention required.

𝟰. 𝗠𝘂𝗹𝘁𝗶-𝗔𝗴𝗲𝗻𝘁 𝗦𝘆𝘀𝘁𝗲𝗺𝘀 (𝗠𝗔𝗦):

- MAS represent the next leap. Multiple agents - each specialized - work together, negotiate, and adapt in real time to achieve shared outcomes across environments.

- FS: Agents handling client onboarding, AML checks, credit assessment, and regulatory filings collaborate seamlessly to approve new clients in minutes.

𝗪𝗵𝘆 𝘁𝗵𝗶𝘀 𝗺𝗮𝘁𝘁𝗲𝗿𝘀:

MAS enable distributed, intelligent systems that can self-organize, learn continuously, and respond dynamically to change. They reduce operational bottlenecks and shift digital architectures from static pipelines to living systems.

𝗜𝗺𝗽𝗹𝗶𝗰𝗮𝘁𝗶𝗼𝗻𝘀 𝗳𝗼𝗿 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗦𝗲𝗿𝘃𝗶𝗰𝗲𝘀:

- Efficiency: MAS collapse multi-day processes into seconds - from KYC to loan origination.

- Mass hyper-personalization: Real-time tailoring of product decisions across customer journeys and risk contexts.

- Resilience: Distributed agents can recover from local failures, reroute tasks, and maintain service continuity without manual intervention.

- Compliance: Agents track regulatory changes and trigger operational updates autonomously.

MAS aren’t just the next step in AI - they’re how AI starts to really work like a system. The real transformation won’t be about bigger models anymore, but about smarter collaboration between them.

Opinions: Panagiotis Kriaris, Graphic source: Capgemini

4) ChatGPT guide

If you’re using ChatGPT, how you prompt makes all the difference. The latest GPT-4.1 guide is out - here are my highlights.

GPT-4.1 brings some 𝗺𝗮𝗷𝗼𝗿 𝗰𝗵𝗮𝗻𝗴𝗲𝘀:

• Instruction Following: More literal and precise responses

• Tool Use: Better integration with APIs and functions

• Long-Context Handling: Can process much larger documents (up to 1 million tokens)

• Multi-Step Workflows: More effective for agent-like tasks and business logic

These are my key prompting takeaways:

🔹 𝗕𝗲 𝗱𝗶𝗿𝗲𝗰𝘁, 𝗯𝗲 𝘀𝗽𝗲𝗰𝗶𝗳𝗶𝗰

The model follows instructions more literally than previous versions. A single clear sentence often fixes unintended behaviour.

🔹 𝗔𝗴𝗲𝗻𝘁𝗶𝗰 𝘄𝗼𝗿𝗸𝗳𝗹𝗼𝘄𝘀

GPT-4.1 is ideal for multi-step tasks. For agents, include reminders to:

• Keep going until the task is solved

• Use tools rather than guessing

• Plan and reflect between steps

🔹 𝗧𝗼𝗼𝗹 𝘂𝘀𝗲 𝗶𝘀 𝘀𝗺𝗮𝗿𝘁𝗲𝗿

Use OpenAI’s tool API directly - no need for workarounds. Clear tool names and concise descriptions improve results.

🔹 𝗣𝗿𝗼𝗺𝗽𝘁𝗶𝗻𝗴 𝗳𝗼𝗿 𝗽𝗹𝗮𝗻𝗻𝗶𝗻𝗴

Want the model to “think aloud”? Ask it to break down tasks step-by-step. This improves accuracy and depth, especially for complex problems.

🔹 𝗟𝗮𝗿𝗴𝗲-𝘀𝗰𝗮𝗹𝗲 𝗶𝗻𝗽𝘂𝘁 𝗵𝗮𝗻𝗱𝗹𝗶𝗻𝗴

It can handle up to 1 million tokens, but performance depends on how you structure the input. Place instructions before the content and keep formatting clean and focused.

🔹 𝗜𝗻𝘀𝘁𝗿𝘂𝗰𝘁𝗶𝗼𝗻 𝗲𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴

Older prompts may not work the same. GPT-4.1 relies less on implied rules—be explicit about desired output, structure, and tone.

𝗕𝗼𝘁𝘁𝗼𝗺 𝗹𝗶𝗻𝗲: GPT-4.1 is highly steerable - but only if you guide it precisely. Build structured prompts, plan agent workflows, and iterate often. Smart prompting is now a skill - and a competitive advantage.

Opinions: Panagiotis Kriaris, Source: GPT-4.1 guide