1) Payment Acceptance Stack 2) Can JPMorgan succeed in Germany? 3) The EU Digital Identity Wallet 4) Compliance as the new moat 5) Can AI replace consultants?

Welcome to my newsletter! Each week a few hand-picked topics from the world of fintech, payments and banking with behind-the-scenes analysis!

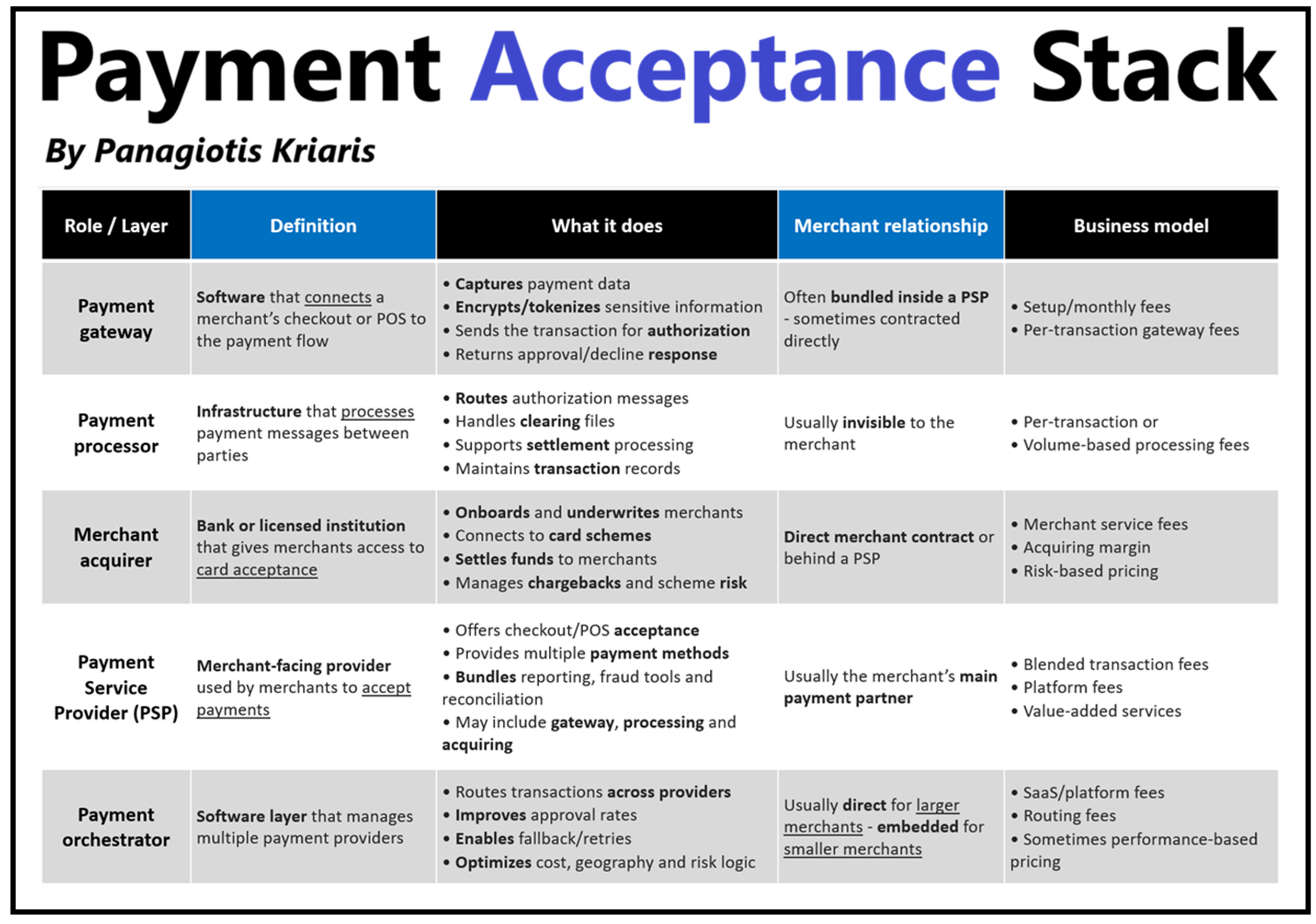

1) Payment Acceptance Stack

Payment acceptance is complex. Gateways, processors, acquirers, PSPs and orchestrators used interchangeably, or bundled together, or even layered on top of each other.

Let’s take a step back.

Whenever we make a payment, online or at POS, a complex flow of communication takes place between merchants, banks and payment networks so that the transaction can be approved and completed in seconds.

This is payment processing.

𝗧𝗵𝗲 𝗿𝗼𝗹𝗲𝘀:

Payment 𝗚𝗮𝘁𝗲𝘄𝗮𝘆:

Software that connects a merchant’s checkout or POS to the payment flow.

• captures and securely transmits payment information

• focuses on the interaction between the merchant environment and the payment infrastructure

Payment 𝗣𝗿𝗼𝗰𝗲𝘀𝘀𝗼𝗿:

The infrastructure that handles the movement of payment information between the different parties involved in a transaction.

• coordinates authorization, clearing and settlement message flows

• operates the high-volume transaction infrastructure behind digital payments

Merchant 𝗔𝗰𝗾𝘂𝗶𝗿𝗲𝗿:

The regulated institution that enables a merchant to accept card payments.

• connects merchants into card scheme ecosystems

• takes responsibility for merchant underwriting, settlement and chargeback exposure

𝗣𝗦𝗣 (Payment Service Provider):

The merchant-facing provider that packages multiple payment capabilities into one solution.

• combines technical, operational and commercial payment capabilities into one service

• simplifies payment acceptance for merchants through a single integration and relationship

Payment 𝗢𝗿𝗰𝗵𝗲𝘀𝘁𝗿𝗮𝘁𝗼𝗿:

The software layer that manages and optimizes multiple payment providers.

• adds a control and routing layer above PSPs and acquirers

• allows merchants to manage provider selection, retries and transaction optimization dynamically

𝗛𝗼𝘄𝗲𝘃𝗲𝗿, 𝘁𝗵𝗲𝘀𝗲 𝗿𝗼𝗹𝗲𝘀 𝗮𝗿𝗲 𝗻𝗼𝘁 𝗮𝗹𝘄𝗮𝘆𝘀 𝘀𝗲𝗽𝗮𝗿𝗮𝘁𝗲:

• Some companies focus on one layer, others combine multiple layers into one offering.

• Many PSPs package gateway, processing and acquiring behind one merchant integration.

• Larger merchants often use multiple PSPs and acquirers instead of relying on a single provider.

• Orchestrators help manage and route transactions across those providers.

• One payment may pass through a gateway, processor, acquirer, card scheme and issuing bank before completion.

𝗧𝗵𝗲 𝘁𝗿𝗲𝗻𝗱𝘀:

• Payments are increasingly moving from single-provider setups to multi-provider stacks focused on resilience, approval performance and cost optimization.

• Intelligence and control are shifting into the orchestration layer as AI, automation and real-time routing make payment decisions increasingly dynamic across multiple providers.

• The market continues to consolidate, with PSPs expanding across gateway, processing, acquiring, fraud and value-added services to control more of the payment stack.

Opinions and graphics: Panagiotis Kriaris

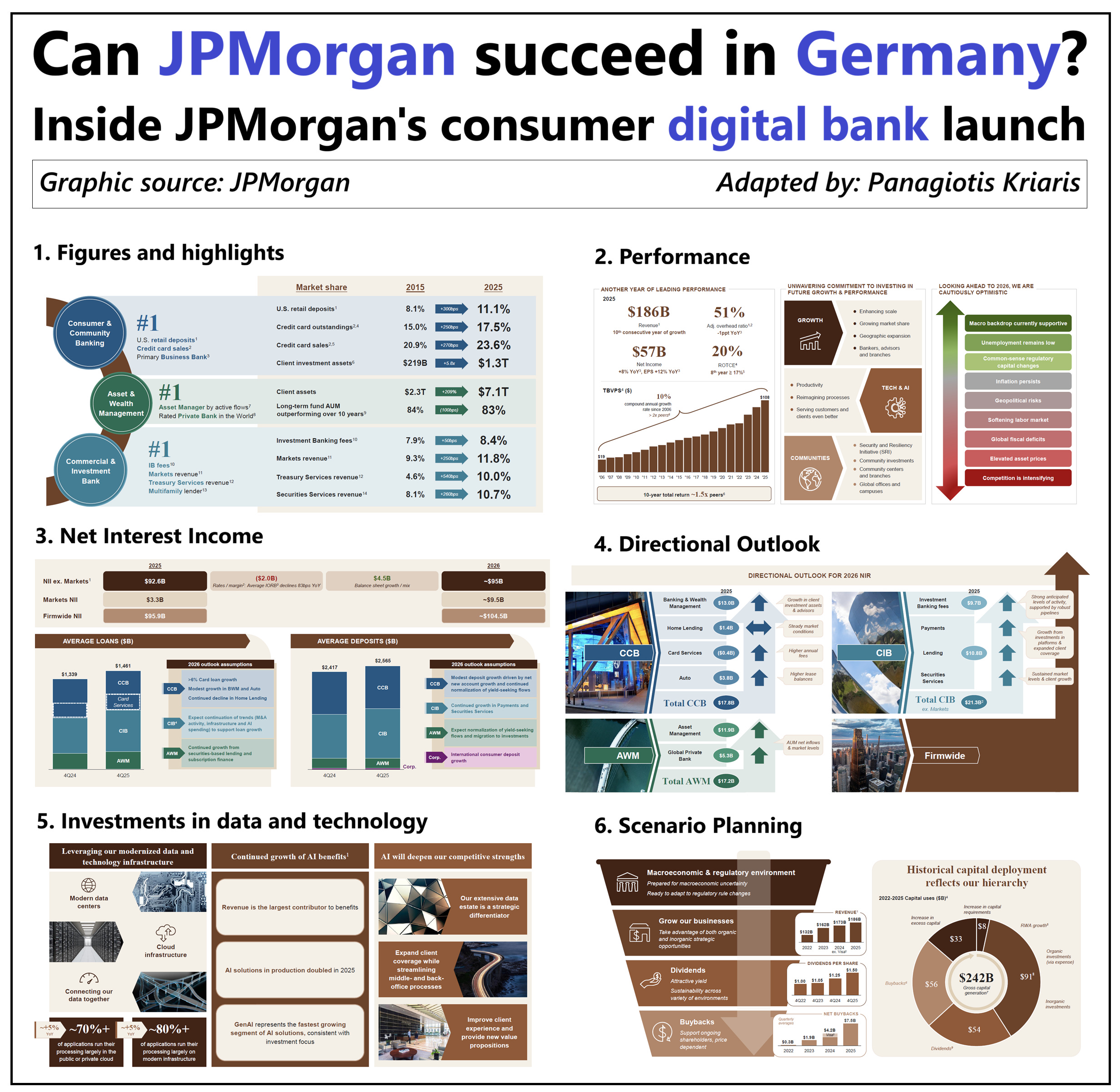

2) Can JPMorgan succeed in Germany?

JPMorgan just launched their consumer digital bank in Germany. It took 3 years. Can they succeed in one of Europe’s toughest banking markets?

JPMorgan wants to replicate the success of its digital bank in the UK.

Since the 2021 UK launch, it has attracted more than 3mn customers and £30bn in deposits.

The launch in Germany consists of just a savings account. With a promotional 4% interest rate for the first 4 months – the market average is 1.32%.

𝗧𝗵𝗲 𝘀𝘁𝗿𝗮𝘁𝗲𝗴𝘆:

• Use aggressive savings rates to rapidly attract deposits.

• Differentiate through intuitive digital experiences and a customer-first proposition.

• Enter with a simpler, lower-friction product instead of asking customers to immediately switch their primary banking relationship.

• Build trust and brand familiarity first before expanding into broader everyday banking services.

• Gradually expand product depth.

𝗕𝘂𝘁 𝗚𝗲𝗿𝗺𝗮𝗻𝘆 𝗶𝘀 𝗮 𝘁𝗼𝘂𝗴𝗵 𝗺𝗮𝗿𝗸𝗲𝘁:

• Europe’s largest economy, with 84 million people, a ~20% savings rate, and more than €10 trillion in household financial assets.

• Customer banking relationships are traditionally very sticky and primary account switching is relatively limited.

• Savings behavior is conservative and trust still plays a major role in consumer banking decisions.

• The market is deeply fragmented across Sparkassen, Volksbanken, direct banks, and large incumbents with around 1,300 banks operating across the country.

• Savings and cooperative banks still control the majority of deposits through strong regional and local presence.

• A large share of household savings still sits in low-yield deposit products despite higher interest rate environments.

• German consumers are more cautious around debt and credit and place emphasis on security and human customer support.

𝗧𝗵𝗲 𝗰𝗵𝗮𝗹𝗹𝗲𝗻𝗴𝗲𝘀:

• Fierce competition from local incumbents, digital banks, and international challengers alike. A promotional savings rate alone is not enough.

• It is famously hard to make money in German banking. Return on equity is among the lowest in Europe, while pricing pressure and conservative customer behavior compress margins.

• Banking in Germany is heavily relationship- and trust-driven. Scaling requires significant localization across onboarding, compliance, servicing, and customer support.

• The economy faces significant structural challenges, including weak growth and pressure on key industrial sectors, which could weigh on consumer sentiment and lending profitability.

• Access to stable customer deposits will be crucial, but they may not come cheap. German savers are highly rate-sensitive and increasingly willing to move large balances for better returns.

• Scale will be difficult. Even a few billions in deposits and hundreds of thousands of customers can still be tiny compared with Deutsche Bank (18mn customers).

Opinions: Panagiotis Kriaris, Graphic source: JPMorgan

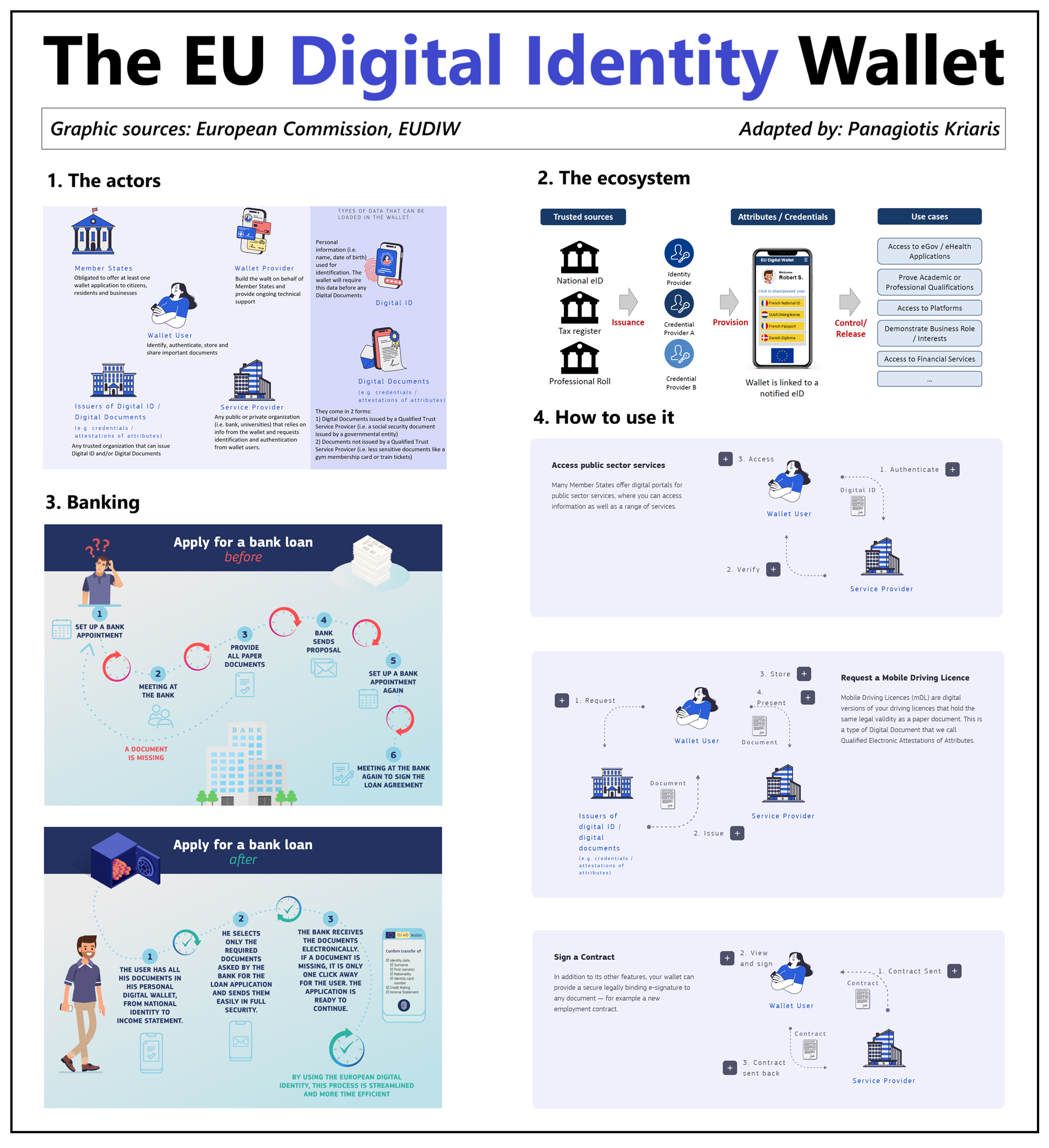

3) The EU Digital Identity Wallet

Digital identity is the new battleground for trust and access to services and the European Digital Identity Wallet (EUDIW) is changing the game.

Digital identity is no longer just about onboarding or logging in.

As services increasingly need reusable, trusted, and interoperable identity to operate across platforms, institutions, and borders, it is becoming the infrastructure layer of the digital economy.

The EUDIW is one of Europe’s most ambitious and forward-looking initiatives in decades.

Many people still have not realized: the rollout starts this year.

𝗕𝘂𝘁 𝘄𝗵𝗮𝘁 𝗶𝘀 𝘁𝗵𝗲 𝗘𝗨𝗗𝗜𝗪?

• A public digital wallet that allows citizens to store and use verified identity credentials across the EU

• Built under the eIDAS 2.0 framework as regulated EU infrastructure

• Enables users to identify themselves, authenticate, sign documents, and share verified credentials digitally

• Designed to work across banking, payments, telecom, healthcare, government services, travel, and e-commerce

• Allows reusable identity instead of repeating onboarding and verification processes across every platform

• Enables cross-border interoperability across the EU

• Creates a foundation for AI agents and digital services

However, 𝘁𝗵𝗲 𝗘𝗨𝗗𝗜𝗪 𝘄𝗶𝗹𝗹 𝗻𝗼𝘁 𝗿𝗲𝗽𝗹𝗮𝗰𝗲 𝗻𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝗶𝗱𝗲𝗻𝘁𝗶𝘁𝘆 𝘀𝗰𝗵𝗲𝗺𝗲𝘀 - it will sit on top of them:

• Identity verification will still come from local providers and national systems in each country

• Different countries will continue using different identity models, standards, and implementations

• The wallet creates a common access layer across Europe but not one unified identity system

• Underneath the European layer, the ecosystem will remain structurally fragmented

𝗪𝗵𝗮𝘁 𝗱𝗼𝗲𝘀 𝘁𝗵𝗶𝘀 𝗺𝗲𝗮𝗻?

Banks, fintechs, and platforms will still need to connect to multiple identity sources across Europe.

All these players have 𝘁𝘄𝗼 𝗼𝗽𝘁𝗶𝗼𝗻𝘀:

𝟭. Build their own technical integration with every EUDI Wallet implementation across all 27 member states.

𝟮. Connect to an orchestration and interoperability provider that can aggregate and normalize fragmented national identity ecosystems.

The first option is not realistic. No one will do that.

Meaning that there is a real interoperability opportunity around simplifying how businesses connect to fragmented national identity ecosystems across Europe.

The difficult part is making fragmented identity systems work together consistently across countries, industries, and institutions.

But not all players are the same. A bank, airline, telecom provider, marketplace, hospital, or government agency may need to consume and trust identity data differently. That creates major complexity around standards, liability, authorization models, credential formats, and cross-border acceptance.

This is why a large part of the future value will sit in the interoperability and orchestration layers that simplify how these fragmented systems connect and operate together.

In many ways, this starts to resemble what card networks did for payments: not replacing banks, but creating a standardized coordination layer between fragmented participants.

80 % of EU citizens are expected to adopt EUDIW by 2030. Financial institutions that treat digital identity as a future topic may already be late.

Opinions: Panagiotis Kriaris, Graphic sources: European Commission, EUDIW

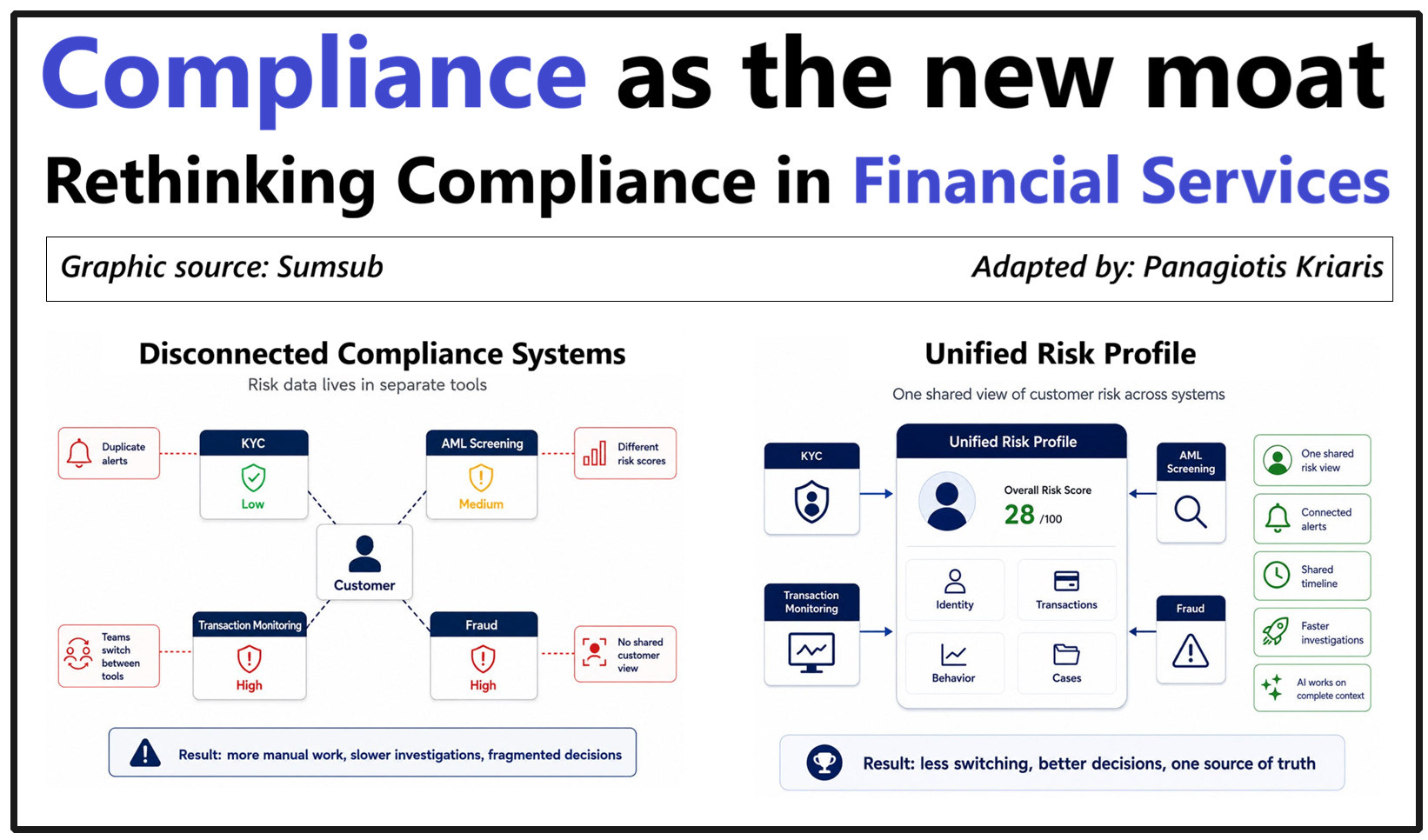

4) Compliance as the new moat

A once overlooked back-office function is becoming one of the biggest competitive moats in financial services.

Compliance is shifting from a regulatory cost center into a real-time intelligence and decisioning layer across onboarding, payments, fraud, risk, and customer operations.

𝗕𝘂𝘁 𝘁𝗵𝗲𝗿𝗲 𝗶𝘀 𝗼𝗻𝗲 𝗽𝗿𝗼𝗯𝗹𝗲𝗺:

Most compliance teams still manage KYC, AML screening, transaction monitoring, fraud, and case management across multiple disconnected systems with no shared view of risk or customer activity.

𝗘𝘅𝗮𝗺𝗽𝗹𝗲𝘀:

• the same customer triggering duplicate alerts across multiple systems

• different tools assigning different risk scores to the same customer

• investigators manually moving across multiple dashboards to understand what is happening

• onboarding, fraud, and AML teams working with different customer data

• no single view of customer behavior, transactions, and risk exposure

• compliance teams spending more time coordinating tools than investigating risk

𝗜𝘀 𝘁𝗵𝗲𝗿𝗲 𝗮 𝘀𝗼𝗹𝘂𝘁𝗶𝗼𝗻?

The industry is already moving toward a unified fincrime prevention platform.

Not by merging tools but by creating a shared intelligence layer across identity, transactions, behavior, investigations, and risk.

𝗪𝗵𝘆?

Because financial crime does not happen in silos. And when compliance operations do, teams lose the ability to connect the dots across the entire customer journey.

The next generation of compliance infrastructure will likely look very different from today’s fragmented model. Instead of separate onboarding, fraud, AML, transaction monitoring, and case management systems operating independently, institutions will move toward unified operational layers with shared customer context, shared investigations, and shared decisioning.

This will change the role of compliance. Institutions that can connect identity, payments, behavior, devices, network relationships, and transaction activity into one operational view will detect patterns faster, reduce false positives, onboard customers quicker, and investigate risk more efficiently.

And as agents start entering compliance operations the transition will becomes even more important. Agents cannot work effectively across fragmented systems and disconnected workflows. Deploying AI on top of disconnected compliance operations means automating fragmented decision-making instead of solving it. Shared context, permissions, traceability, and connected workflows will become foundational infrastructure for how future compliance operations function.

𝗥𝗲𝘁𝗵𝗶𝗻𝗸𝗶𝗻𝗴 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲 𝗶𝘀 𝘁𝗵𝗲 𝗻𝗲𝘄 𝗺𝗼𝗮𝘁.

Opinions: Panagiotis Kriaris, Graphic source: Sumsub

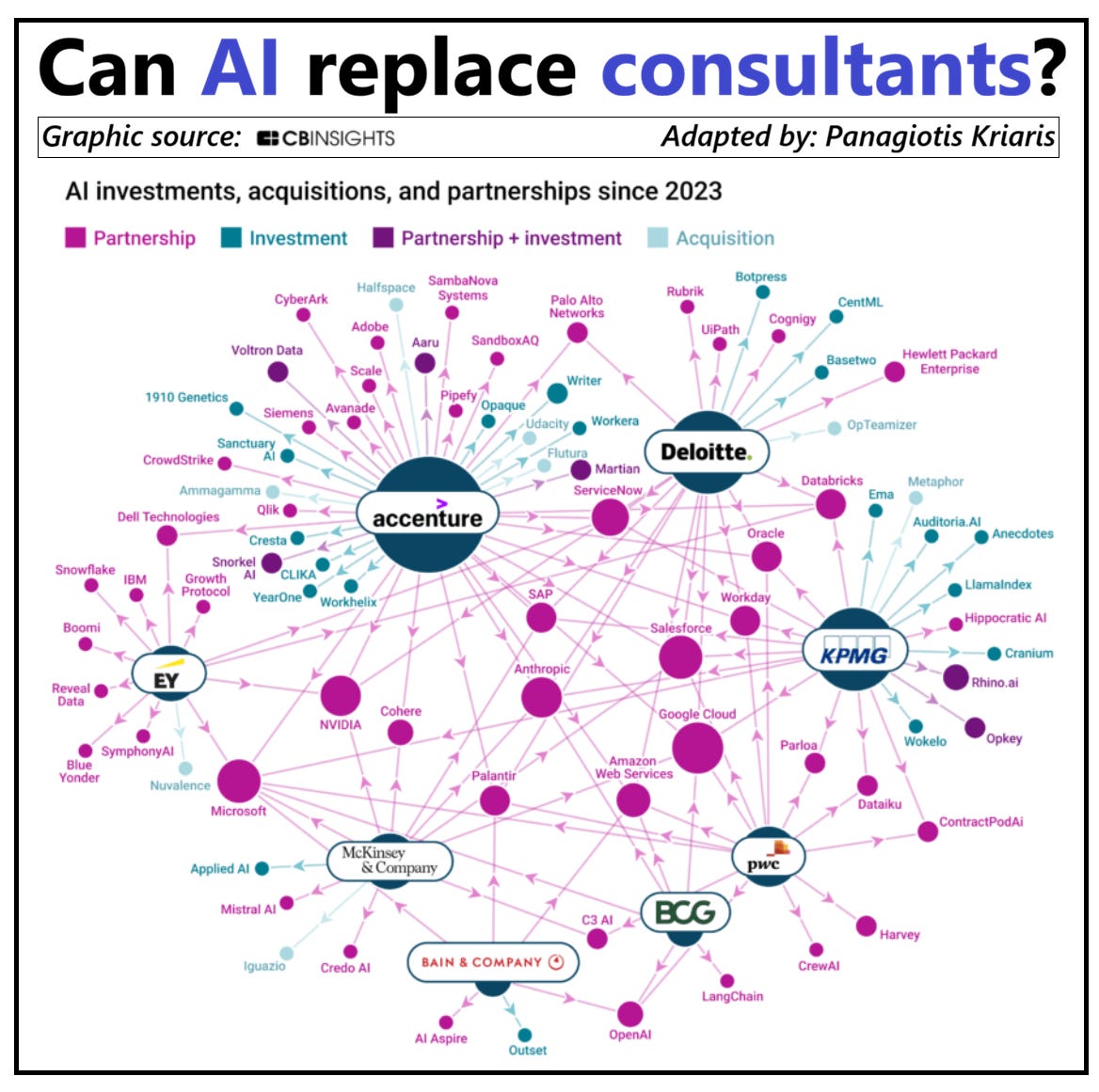

5) Can AI replace consultants?

McKinsey has 40,000 employees and 25,000 AI agents. Now it is adjusting remuneration to AI. An entire industry is being disrupted by AI. And it is not the only one.

Less than 2 years ago McKinsey had just 3,000 AI agents. Its CEO originally expected to reach one AI agent per employee by 2030. Now it might be months away.

𝗕𝘂𝘁 𝘄𝗵𝗮𝘁 𝗱𝗼 𝗮𝗴𝗲𝗻𝘁𝘀 𝗱𝗼 𝗶𝗻 𝗰𝗼𝗻𝘀𝘂𝗹𝘁𝗶𝗻𝗴?

• Consulting is full of work that is structured, repeatable, research-heavy, and analysis-driven. Exactly the type AI can replace.

• Agents can help consultants search internal knowledge, summarize documents, compare markets, draft first versions, structure analyses, test hypotheses, build models, prepare client materials, and accelerate the kind of linear problem-solving that used to consume large amounts of junior consultant time.

This does not mean McKinsey no longer needs consultants.

It means consulting is changing.

If AI can produce the first draft, the benchmark, the synthesis, the model, or the analysis, humans have to become better at the parts AI cannot reliably do:

• setting the right ambition

• applying judgment

• challenging answers

• managing the client

• connecting politics with strategy

• turning analysis into decisions

This is much bigger than automation.

Consulting firms are now redesigning the economics of consulting around a new execution layer.

𝗟𝗲𝘁’𝘀 𝘁𝗮𝗸𝗲 𝗼𝗻𝗲 𝘀𝘁𝗲𝗽 𝗯𝗮𝗰𝗸.

For decades, the consulting model was built around senior partners selling the work, large teams delivering it, and clients paying for expertise, time, and execution capacity.

If now AI agents are doing an increasing part of this work, clients will ask why they should pay the same way for work that now takes less human effort.

That means consulting firms need to adjust their business model: from selling hours and advice to selling outcomes.

Savings, cost reduction, productivity improvement, revenue increase, real transformation.

𝗧𝗵𝗶𝘀 𝗶𝘀 𝘄𝗵𝗮𝘁 𝗠𝗰𝗞𝗶𝗻𝘀𝗲𝘆 𝗶𝘀 𝗰𝗵𝗮𝗻𝗴𝗶𝗻𝗴 𝗻𝗼𝘄:

Partners will receive a smaller share of profits in cash and a larger share in equity. In practice, part of the money that would have been paid out immediately stays inside the firm.

𝗪𝗵𝘆?

• Because consulting cash flows may become more volatile. If more projects are tied to savings or performance improvements, the firm may only get fully paid once the client actually delivers the result.

• McKinsey needs more capital inside the business: to absorb delayed payments, take more outcome risk, and invest in the technology needed to deliver work differently.

Consulting companies are adopting 𝗼𝘂𝘁𝗰𝗼𝗺𝗲-𝗯𝗮𝘀𝗲𝗱 𝗽𝗿𝗶𝗰𝗶𝗻𝗴.

Any industry built on expensive expert work, repeatable analysis, and billable hours will face the same pressure: to move from selling activity to selling outcomes.

Opinions: Panagiotis Kriaris, Graphic source: CB Insights