1) Open Banking Architecture 2) GenAI vs Agentic AI 3) The Platform Bank Model

Welcome to my newsletter! Each week 2-3 hand-picked topics from the world of fintech, payments and banking with behind-the-scenes analysis!

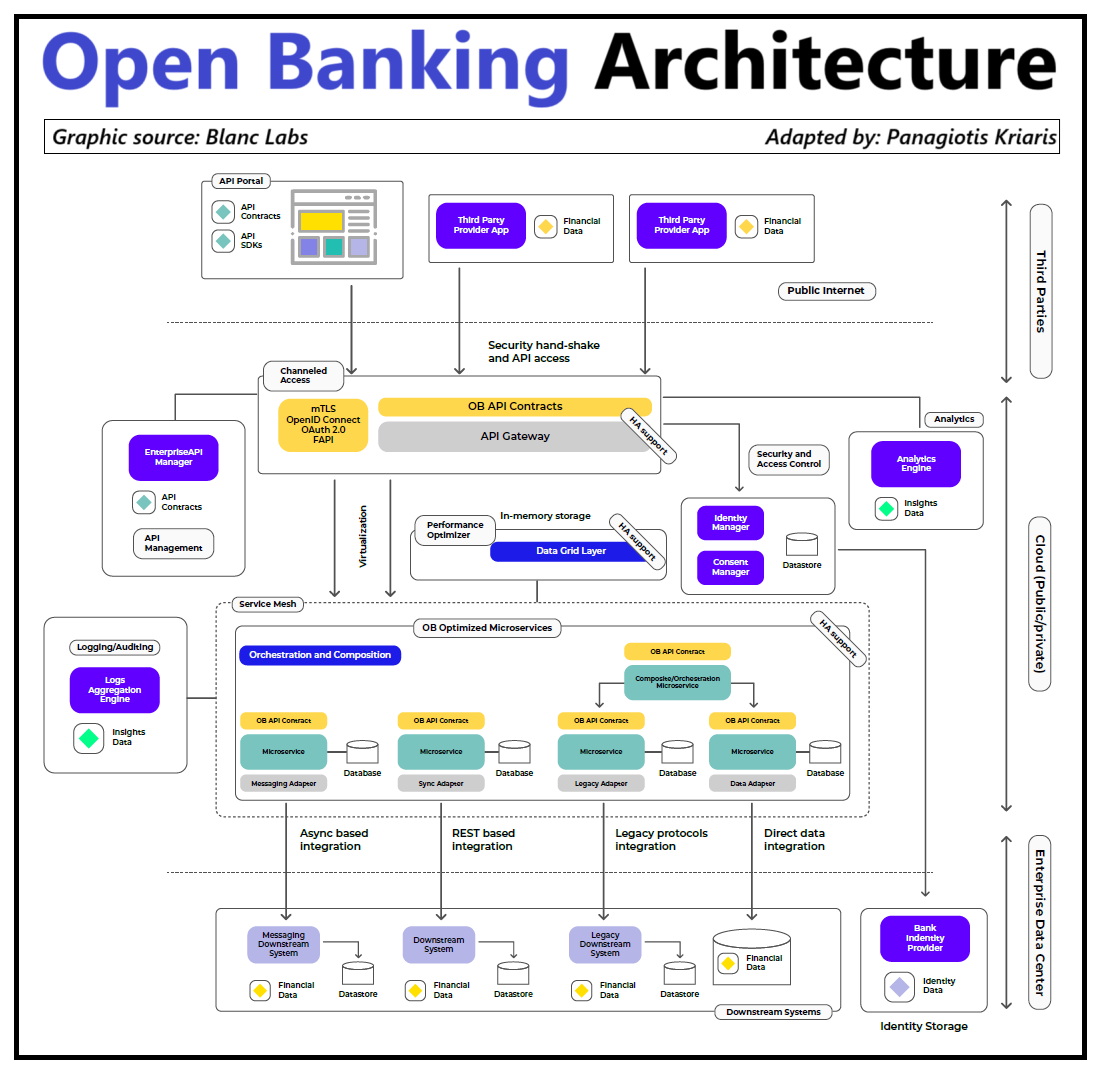

1) Open Banking Architecture

Open Banking (OB) isn’t a feature - it’s the blueprint for banks to stay relevant in an APIsed economy. But exposing a few APIs is not innovation. Here's what really powers OB - and some myth busting.

OB is reshaping how we access and interact with financial services. At its core, it’s about unlocking data and making it securely available through modern infrastructure rails called APIs.

But the impact goes far beyond banking. OB is becoming the key enabler of today’s two most dominant business models:

— Platform economics

— Embedded finance

Banks play a critical role in this shift - because they hold the data.

Enter: 𝗢𝗽𝗲𝗻 𝗕𝗮𝗻𝗸𝗶𝗻𝗴 𝗔𝗿𝗰𝗵𝗶𝘁𝗲𝗰𝘁𝘂𝗿𝗲

This is the invisible technical foundation that allows banks to expose data and services to fintechs and partners. Here’s a simplified breakdown of key components:

1. API Gateway – The secure front door that handles requests and and routes them properly.

2. Consent & Identity Management – Ensures only the right parties get access, with the customer’s permission.

3. Authentication Layer – Uses secure login methods to confirm the customer’s identity.

4. Developer Portal – A gateway where third parties discover, test, and onboard to the bank’s APIs.

5. Microservices Layer – Breaks banking functions into modular services for faster, flexible delivery.

6. Core System Integration – Connects modern APIs to banks’ legacy systems without needing to rebuild everything from scratch.

This isn’t just about technology - it’s about designing trust at scale.

𝗛𝗼𝘄 𝗮𝗻 𝗢𝗽𝗲𝗻 𝗕𝗮𝗻𝗸𝗶𝗻𝗴 𝗿𝗲𝗾𝘂𝗲𝘀𝘁 𝘄𝗼𝗿𝗸𝘀:

1. A licensed third-party provider (TPP) sends an API request to the bank to access account data or initiate a payment.

2. The end-user is redirected to the bank’s interface to authenticate and provide consent.

3. Once consent is verified, the bank issues a secure access token to the TPP.

4. The TPP retrieves only the authorized data or completes the payment transaction.

5. All actions are logged for traceability, audit, security and compliance purposes.

𝗪𝗵𝗮𝘁’𝘀 𝗵𝗼𝗹𝗱𝗶𝗻𝗴 𝗯𝗮𝗻𝗸𝘀 𝗯𝗮𝗰𝗸?

1. Legacy tech – Many core platforms were never built for external connectivity.

2. Security & compliance pressure – Exposing APIs while meeting regulatory requirements is complex.

3. Real-time readiness – Open Banking requires real-time availability and minimal downtime.

4. Governance and ecosystem management – Managing third-party access and maintaining oversight is operationally demanding.

Banks should avoid treating OB as just a tech upgrade or a compliance checkbox. It’s a strategic opportunity to modernize infrastructure - something they would have to do anyway. In the era of AI and real-time digital ecosystems, not being able to communicate via APIs is like owning a smartphone without internet access.

Opinions: my own, Graphic source: Blanc Labs

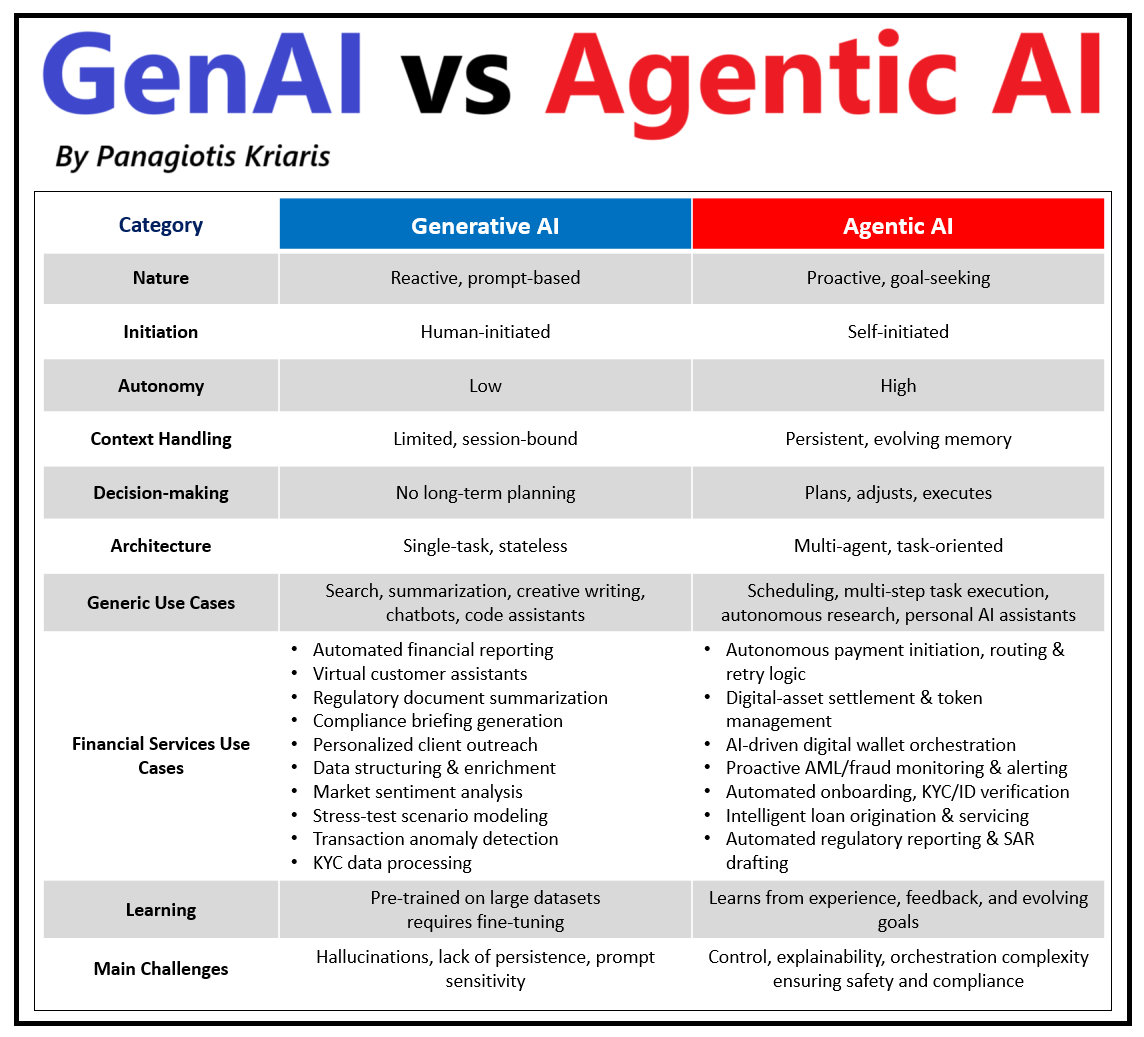

2) GenAI vs Agentic AI

Just a year ago it was all about GenAI. Today the spotlight is on Agentic AI. What is driving the shift?

𝗗𝗲𝗳𝗶𝗻𝗶𝘁𝗶𝗼𝗻

- GenAI: Models that create or transform content in response to prompts.

- Agentic AI: Systems that can pursue goals, plan tasks, and take action with minimal human input.

GenAI helps generate ideas; Agentic AI takes action and gets things done.

𝗚𝗲𝗻𝗔𝗜 𝘀𝘁𝗿𝗲𝗻𝗴𝘁𝗵𝘀

- Rapid content & pattern creation

- Natural‑language front ends for analytics

Finance examples

• Auto‑drafted research and client letters

• Multilingual regulatory summaries

• Synthetic stress‑test narratives

𝗔𝗴𝗲𝗻𝘁𝗶𝗰 𝗔𝗜 𝘀𝘁𝗿𝗲𝗻𝗴𝘁𝗵𝘀

• Real‑time decisioning under uncertainty

• Multi‑skill chaining (retrieve → reason → act)

• Continuous learning from outcomes

Finance examples

• Millisecond fraud-blocking on millions of card transactions

• Dynamic risk-rule tuning based on issuer feedback

• Automated receivables follow-up and payment posting

• Autonomous treasury operations: FX hedging and overnight liquidity management

𝗪𝗵𝘆 𝘁𝗵𝗲 𝘀𝗵𝗶𝗳𝘁

Moving from GenAI to Agentic AI fundamentally changes how financial services deliver value:

• Real-time revenue protection: agentic systems can reroute or block high-risk payments instantly, slashing fraud losses and chargebacks.

• Seamless customer journeys: fully automated KYC and onboarding flows.

• Dynamic liquidity management: treasury bots rebalance cash, execute FX hedges, and optimize funding costs overnight.

• End-to-end payment orchestration from choosing the most cost-effective cross-border rail to retrying failed pay-outs.

• Regulatory agility: continuous-monitoring agents track rule changes, update compliance workflows, and generate audit trails without manual intervention.

𝗪𝗵𝗮𝘁’𝘀 𝗻𝗲𝘅𝘁

• Conversational banking agents: go beyond answering questions - initiate transfers, set up recurring payments, and negotiate loan terms.

• Embedded Finance at scale: agents orchestrate lending, insurance, and FX in real time within non-financial apps.

• On-demand cross-border settlement: smart agents choose between CBDCs, stablecoins, or traditional rails to settle payments instantly at the lowest cost.

• Predictive risk & credit scoring: continuously update merchant and counterparty scores as new data streams in.

• Auto-remediating systems: agents detect and fix platform issues in real time - no human ops required.

• Automated regtech: agentic workflows handle licensing, screening, reporting, and audits - cutting compliance time from weeks to hours.

• AI treasury market making: bots quote and underwrite liquidity in real time, adjusting spreads dynamically to market shifts.

Opinions: my own

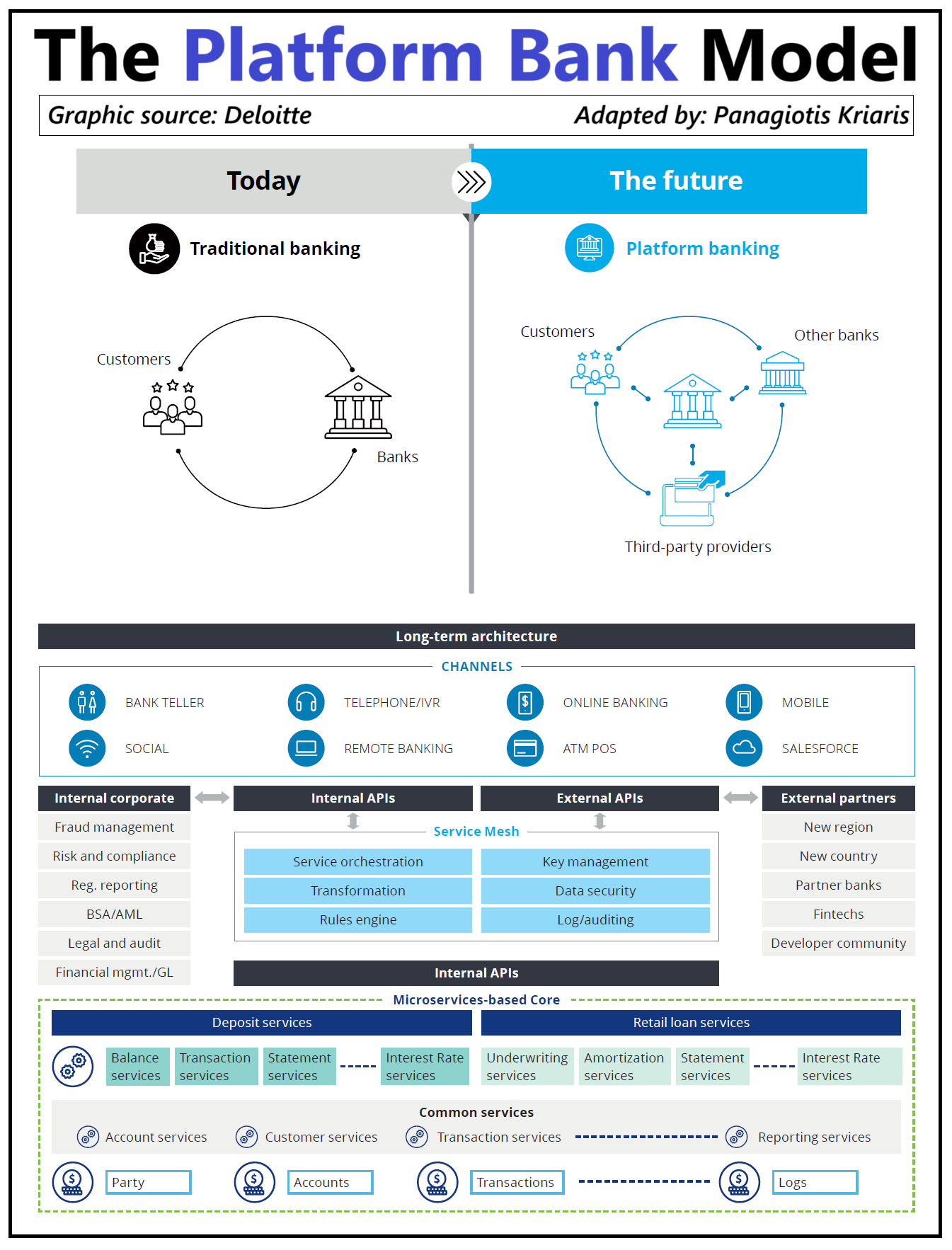

3) The Platform Bank Model

Banks aren’t fighting for market share anymore – they are fighting for relevance. In the age of platforms, control has shifted from infrastructure to distribution. How can they adjust?

𝗧𝗵𝗲 𝗯𝗶𝗴 𝘀𝗵𝗶𝗳𝘁:

One of the biggest triggers in the transition to the platform economy has to do with the shift from infrastructure ownership to control of the customer relationship as the single most important success factor. For decades, competition was shaped by the back end - today, it’s the front end that holds the power.

For banks, adapting to this reality is inevitable. In fact, many banks claim they either have or are working on a platform strategy. But size, market, and regulation prevent them from copying the BigTech playbook.

𝗦𝗼, 𝘄𝗵𝗮𝘁 𝗰𝗮𝗻 𝗯𝗮𝗻𝗸𝘀 𝗱𝗼?

- As a starting point, banks need to change their vertically integrated and product-focused approach to an open set-up that is built on integrating third-party and fintech offerings via APIs.

- Getting their API strategy right is critical, given that platformification is nothing more than a well-orchestrated ecosystem of interconnected products and services (not necessarily their own) glued together by means of APIs.

The more successful they are in this strategy, the higher up they can move in the digital value chain and become entangled in their customers’ day-to-day, resulting in new revenue pools.

𝗧𝗵𝗲 𝗻𝗲𝘄 𝗶𝗻𝗳𝗿𝗮𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲:

A microservices-based architecture can providing the flexibility and speed that platform banking demands:

- Small, autonomous services each focused on a distinct business domain

- Plug-and-play integration of fintech and partner offerings without core rewrites

- Accelerates experimentation, innovation and time-to-market

- Enables banks to personalize experiences and pivot rapidly

𝗠𝗮𝗶𝗻 𝗰𝗵𝗮𝗿𝗮𝗰𝘁𝗲𝗿𝗶𝘀𝘁𝗶𝗰𝘀:

1. Systems are split into small, self-contained services that own their data, cutting dependencies.

2. Each service updates on its own timeline, so one change never holds up the rest.

3. A central gateway directs outside requests and keeps things secure, while an internal layer handles how units talk to each other.

4. Services auto-scale based on load and isolate failures to prevent system-wide outages.

5. Automated workflows build, test, and release updates quickly with minimal risk.

6. Unified monitoring provides a single view for spotting and fixing issues.

7. Security rules apply to each service individually, limiting any breach to a small area.

8. Automatic scaling and right-sized resources ensure usage and costs match actual needs.

Opinions: my own, Graphic source: Deloitte

Sadly, most banks still see OB as a door through which fintech will enter to steal their marketshare…