1) Can Open Banking replace Cards? 2) The UK Apple Pay Battle 3) Banks' next IT transformation 4) The Capital One-Brex Deal

Welcome to my newsletter! Each week a few hand-picked topics from the world of fintech, payments and banking with behind-the-scenes analysis!

1) Can Open Banking replace Cards?

Can Open Banking replace cards? And what are the deciding factors?

To answer the question, we need to understand the mechanics behind each model.

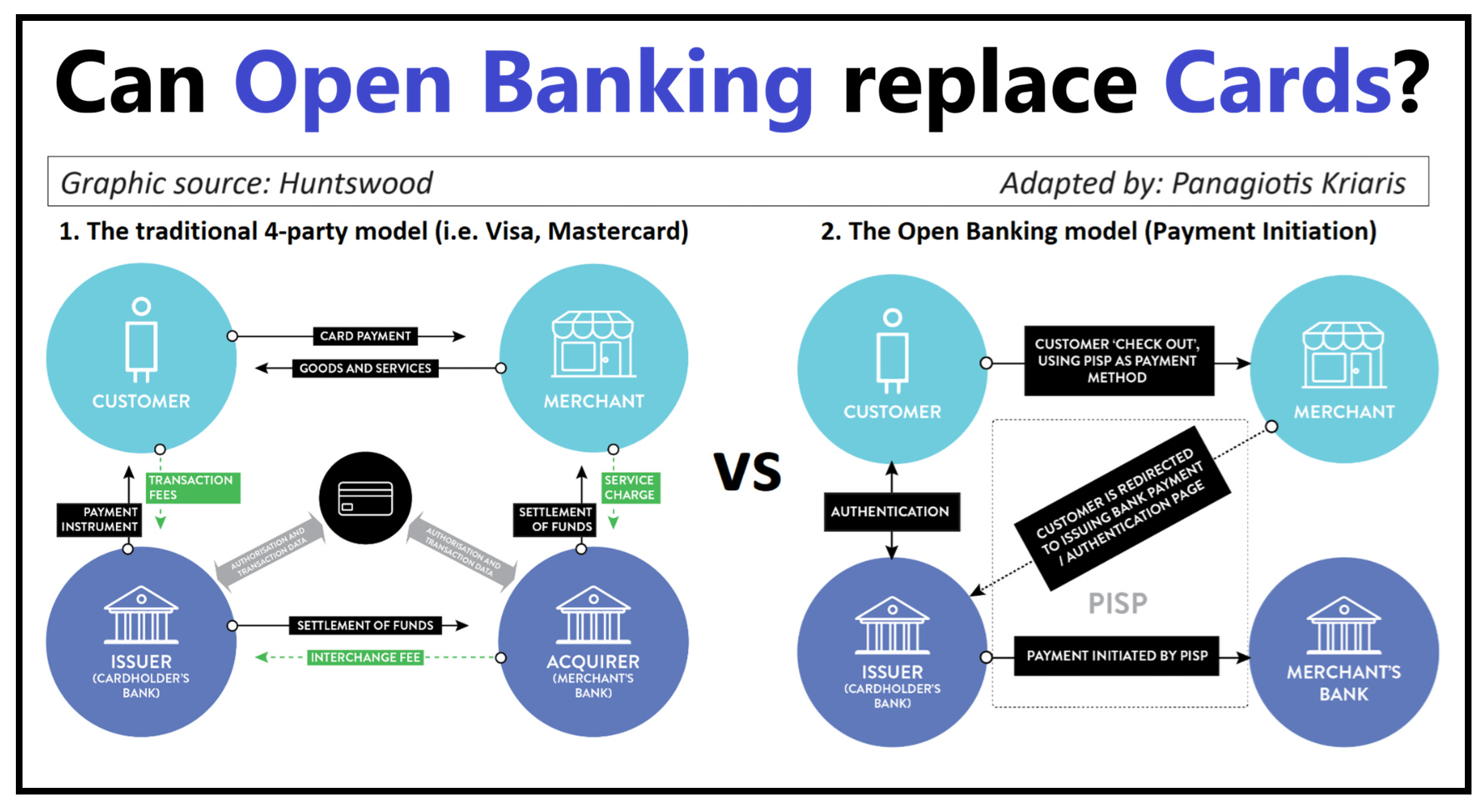

𝗧𝗵𝗲 𝘁𝗿𝗮𝗱𝗶𝘁𝗶𝗼𝗻𝗮𝗹 𝟰-𝗽𝗮𝗿𝘁𝘆 𝗺𝗼𝗱𝗲𝗹 (𝗩𝗶𝘀𝗮, 𝗠𝗮𝘀𝘁𝗲𝗿𝗰𝗮𝗿𝗱):

A typical transaction flow would look like this:

𝟭. A third-party (merchant) gateway identifies the right payment network

𝟮. The (card) network confirms the customer authorization

𝟯. The network routes the transaction to the customer’s bank (the issuer) for approval

𝟰. The network does the same with the merchant’s bank (the acquirer)

𝟱. After the approvals the gateway confirms the transaction

𝟲. The merchant’s bank settles with the network, whereas payment is done by the customer’s bank

For this middleman role, card networks define access fees (the costs for routing a card payment through their network) and interchange fees that merchants pay to the card issuers.

The latter can range from 0.3% for credit cards in Europe (there is a cap) and all the way up to 3.5% in the US and Canada (the most expensive in the world).

On the other hand, Open Banking can be a game changer because it connects merchants with consumers in a direct way, without intermediaries: payments are initiated directly from the consumer’s bank account.

𝗧𝗵𝗲 𝗢𝗽𝗲𝗻 𝗕𝗮𝗻𝗸𝗶𝗻𝗴 𝗺𝗼𝗱𝗲𝗹:

𝟭. The customer chooses ‘Pay by bank’ at checkout and selects the bank

𝟮. The transaction is redirected to the customer’s banking app

𝟯. The transaction is approved, and the merchant is notified

𝗪𝗵𝗮𝘁 𝘀𝗽𝗲𝗮𝗸𝘀 𝗶𝗻 𝗳𝗮𝘃𝗼𝘂𝗿 𝗼𝗳 𝗢𝗽𝗲𝗻 𝗕𝗮𝗻𝗸𝗶𝗻𝗴:

• PIS payments cost a fraction of cards, while delivering strong security, smoother UX, and near-instant settlement as real-time schemes scale globally

• Margin pressure is forcing change. As competition intensifies, merchants are actively looking for cheaper ways to accept and move money

• Open Banking is powering for the first time in a long period the build-up of a real, additional infrastructure layer that has the potential to influence the entire finance set-up.

𝗪𝗵𝗮𝘁 𝘀𝗽𝗲𝗮𝗸𝘀 𝗶𝗻 𝗳𝗮𝘃𝗼𝘂𝗿 𝗼𝗳 𝗰𝗮𝗿𝗱𝘀:

• Cards don’t just enable payments; they fund rewards, cashback, insurance, and loyalty ecosystems that actively shape consumer behaviour and are hard to sustain on low-margin A2A rails

• Decades of investment have built a dense card infrastructure - fraud management, disputes, tokenisation, wallets, and seamless checkout - that cannot be replicated easily

• Cards remain unmatched in global, cross-border, and offline acceptance, while open banking is still largely domestic

• Strong network effects and consumer habits keep cards embedded in everyday payments

𝗧𝗵𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻:

What are the lessons learned from Open Banking’s trajectory around the globe so far?

Opinions: Panagiotis Kriaris, Graphic source: Huntswood

2) The UK Apple Pay Battle

This goes beyond digital wallets. The legal action against Apple in the UK is just the tip of the iceberg behind a complex structure spanning platforms, wallets, payments - and who is really in charge.

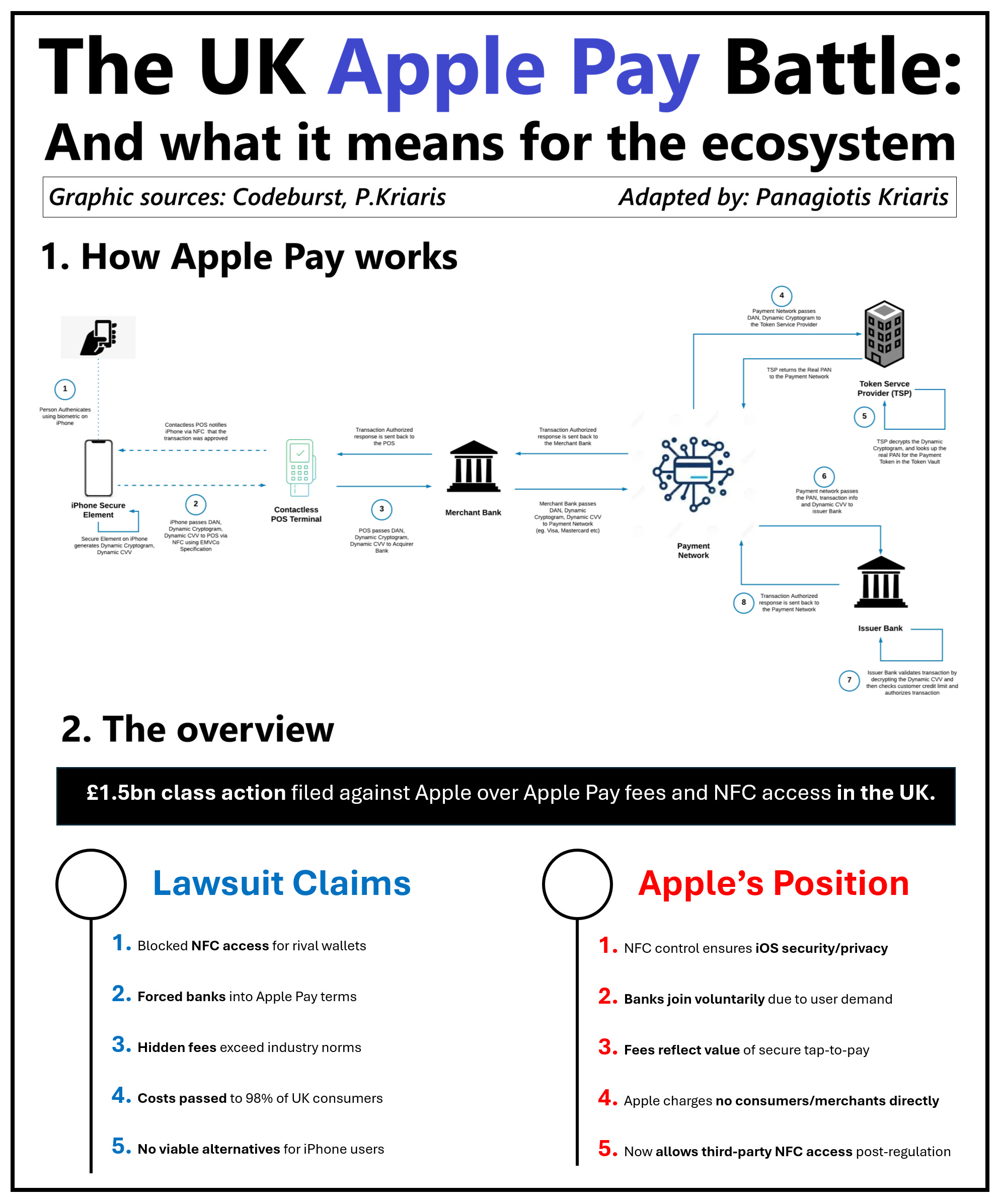

Apple has built a unique ecosystem:

• Apple Wallet is the built-in wallet on the iPhone, used to store payment cards.

• Apple Pay is the payment service that uses those cards to initiate contactless payments when an iPhone is tapped at a terminal.

• For that tap to work, the iPhone uses NFC, and Apple defines how wallets can access it through the operating system.

• Because Apple Pay is built into iOS, every iPhone tap-to-pay transaction is initiated inside Apple’s software before it reaches the bank or card network.

• Banks issue the cards, move the money and carry fraud risk, but must connect to Apple Pay to reach iPhone users.

• Only after Apple Pay has initiated the transaction does it travel to card networks and then to the merchant’s bank for processing and settlement.

What does this mean?

• This means Apple controls the starting point of the transaction, giving it influence over access, rules and economics - even though it never moves the money itself.

• The CMA has previously scrutinised Apple’s role as the iOS platform owner, including its control over NFC access for tap-to-pay.

• The issue is not Apple Pay as a consumer product, but Apple acting as a gatekeeper between users, wallets and the wider payments ecosystem.

What is the new legal case about?

• A new £1.5bn UK legal action challenges Apple’s role as the de facto gateway for iPhone contactless payments.

• It argues that banks have no commercially viable alternative but to accept Apple’s wallet terms if they want to reach iPhone users.

• As a result, fees and conditions set at the wallet layer are said to distort competition and spread costs across consumers, including those who do not use Apple Pay.

Apple’s position

• Apple says Apple Pay is optional and that banks are not forced to participate, arguing that participation reflects demand from iPhone users rather than lack of choice.

• It maintains that it does not charge consumers or merchants, and that any fees paid by banks reflect the value of enabling secure tap-to-pay transactions on iPhones.

• Apple argues that its control of tap-to-pay and NFC access is necessary to maintain security, privacy and system integrity on iOS.

• It points to recent changes allowing third-party wallets to access NFC and offer tap-to-pay functionality on iPhones, following regulatory scrutiny in the UK and EU.

This is a case that will not just test what happens with Apple, but how control at the wallet and device layer is treated across the wider platform economy.

What do you think happens next?

Opinions: Panagiotis Kriaris, Graphics: Codeburst, Panagiotis Kriaris

3) Banks’ next IT transformation

It’s a paradox: banks have spent decades - and billions - trying to make their core systems intelligent. Now AI is moving intelligence out of those systems.

Banks spend around $650 billion every year on IT and digital transformation (McKinsey) - the size of Belgium’s GDP.

But how much of that spending has translated into measurable outcomes - ROI, growth, or better UX?

Not as much as the scale of investment suggests.

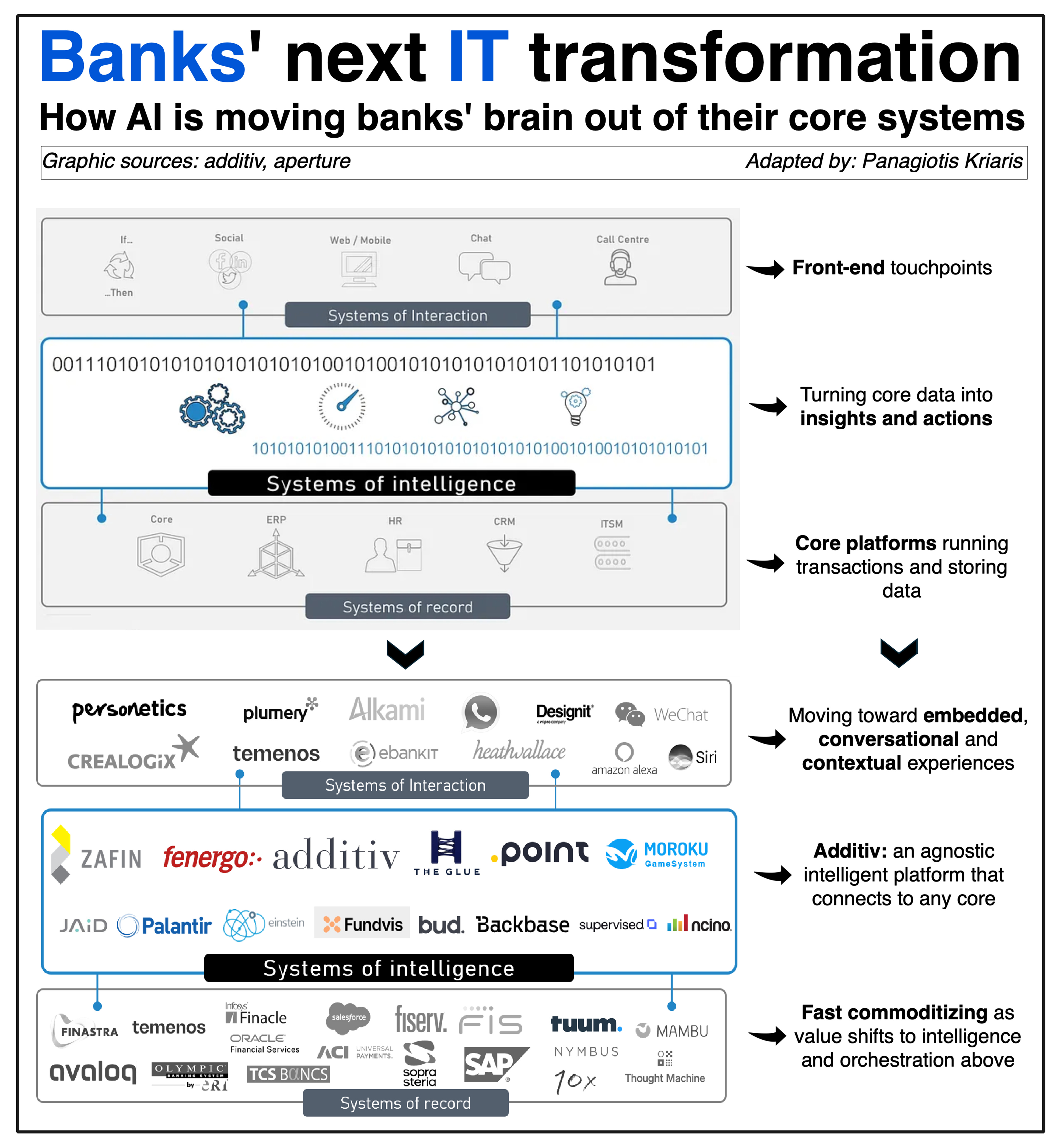

The challenge for banks is that this is no longer where transformation happens. AI is shifting value one layer above the core - in what used to be middleware, now evolving into an intelligence layer.

𝗪𝗵𝘆?

Because the core was never built for flexibility, but for reliability, control, and compliance. It’s designed to execute predefined rules, not to adapt or make new decisions - which is why intelligence is now moving one layer up.

𝗪𝗵𝗮𝘁 𝗱𝗼𝗲𝘀 𝘁𝗵𝗶𝘀 𝗺𝗲𝗮𝗻 𝗳𝗼𝗿 𝗯𝗮𝗻𝗸𝘀?

To capture this new value, banks must rethink transformation.

It’s no longer about replacing what works at the core, but about building intelligence on top of it.

In practice, this requires:

𝟭) Refocusing from core modernisation to intelligence enablement.

𝟮) Treating AI not as automation alone, but as a reasoning layer that connects strategy, operations, and experience.

𝟯) Embedding compliance, explainability, and control.

This is where a new breed of companies comes in - bridging the gap between static core infrastructure and real-time intelligence.

additiv is a prime example, having built an agnostic agentic and domain-specific intelligence layer - a platform that works with any core, adding reasoning, orchestration, and learning into banks’ existing frameworks with human oversight. It’s showing the way forward for operationalizing agentic AI in financial services.

𝗛𝗼𝘄 𝗶𝘁 𝘄𝗼𝗿𝗸𝘀:

• System integration: Connects core, CRM, risk, and channel systems, keeping data consistent and product information aligned across lending, savings, insurance and wealth.

• Product delivery: Enables new propositions without touching the core - e.g., combining savings and investments or embedding credit at POS.

• Decisioning and personalisation: Uses customer data to recommend the next best product, adjust limits, or trigger advice.

• Compliance & governance: Auditability, explainability, and regulatory consistency across AI-driven outcomes.

• Innovation: New use cases - e.g. dynamic pricing, x-product bundles - can be deployed in weeks, reusing existing data and logic.

• Intelligent automation: applying domain rules, and semantically transformed data to orchestrate complex processes, e.g. E2E insurance claims.

The banks’ brains are moving outside the core. That’s only a threat if banks don’t react - for those that do, it’s an opportunity to gain flexibility and multiply the return on their IT investment.

Opinions: Panagiotis Kriaris, Graphic sources: additiv, Aperture

4) The Capital One-Brex Deal

It’s the largest bank–fintech acquisition of all time. Capital One buying Brex is not just an M&A deal. Here’s what you won’t find in the headlines.

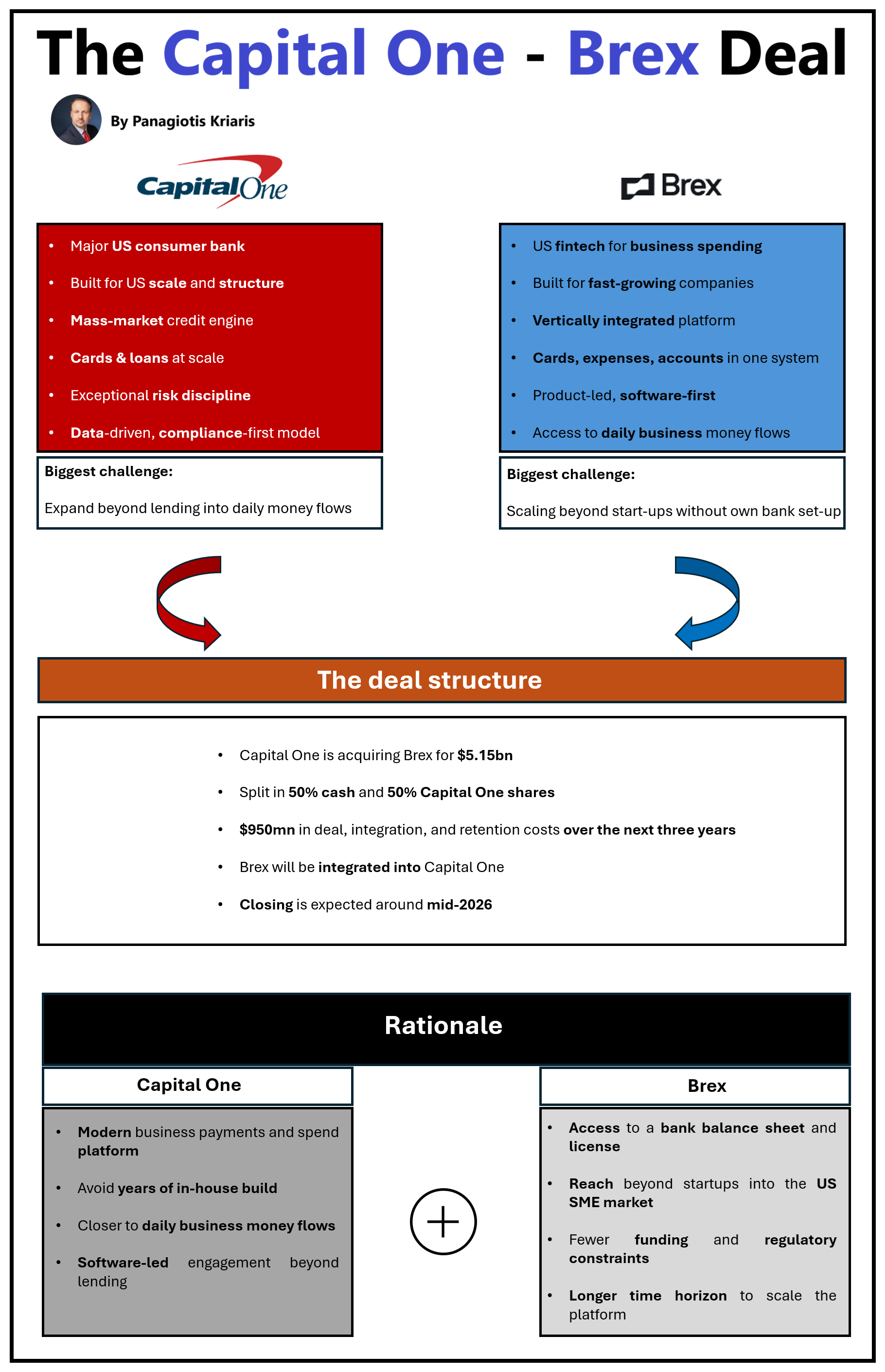

𝗪𝗵𝗼 𝗶𝘀 𝗖𝗮𝗽𝗶𝘁𝗮𝗹 𝗢𝗻𝗲:

• A major US consumer bank, built for the US scale and structure

• Its core strength is mass-market credit: issuing cards and loans at scale and managing risk with exceptional discipline

• Data-driven, highly standardised, compliance-first model

𝗪𝗵𝗼 𝗶𝘀 𝗕𝗿𝗲𝘅:

• A US fintech that runs a software platform to control and automate employee spending

• Built as a vertically integrated platform, combining corporate cards, spend management, and banking into a single system

𝗧𝗵𝗲 𝗱𝗲𝗮𝗹 𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲:

• Capital One is acquiring Brex for $5.15bn

• Split in 50% cash and 50% Capital One shares

• $950m in deal, integration, and retention costs over the next three years

• Brex will be integrated into Capital One

• Closing is expected around mid-2026

𝗖𝗮𝗽𝗶𝘁𝗮𝗹 𝗢𝗻𝗲 𝗿𝗮𝘁𝗶𝗼𝗻𝗮𝗹𝗲:

• Gets access to a modern business payments and spend platform that would take years to build inside a regulated bank

• Shifts Capital One closer to daily business money flows (payments, spend, accounts)

• Adds software-led distribution and higher engagement with SMEs, beyond traditional lending

• Brex brings a proven operating model for product speed and iteration that complements Capital One’s risk and compliance strengths

𝗕𝗿𝗲𝘅 𝗿𝗮𝘁𝗶𝗼𝗻𝗮𝗹𝗲:

• Brex gains access to a large, stable balance sheet and a regulated banking infrastructure, instead of relying on partner banks

• Capital One provides distribution into the mainstream US SME market, beyond startups and tech companies

• Removes funding and regulatory constraints, letting Brex focus on product, platform, and workflow depth

• Being embedded inside a major bank gives Brex stability: longer time horizons, lower risk tolerance, and room to scale its model more broadly

𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝘆 𝗶𝗺𝗽𝗹𝗶𝗰𝗮𝘁𝗶𝗼𝗻𝘀:

• The deal adds to the evidence that build-vs-buy is no longer a real debate for banks

• Software and workflows are becoming more strategic than balance sheets in business banking

• Fintechs that sit in daily money flows are more valuable than those that only optimise financial products

• Regulation and scale still matter - but they now need to be paired with product speed and software depth

• The next phase of fintech consolidation will be about adding capabilities

𝗧𝗵𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻:

What is the biggest challenge that threatens the value of this deal?

Opinions and graphics: Panagiotis Kriaris