1) Banking Platform Evolution 2) Vertical AI models 3) Finance Technology Trends 4) Anatomy of AI Agents 5) Big Banks' Tokenization Bet

Welcome to my newsletter! Each week a few hand-picked topics from the world of fintech, payments and banking with behind-the-scenes analysis!

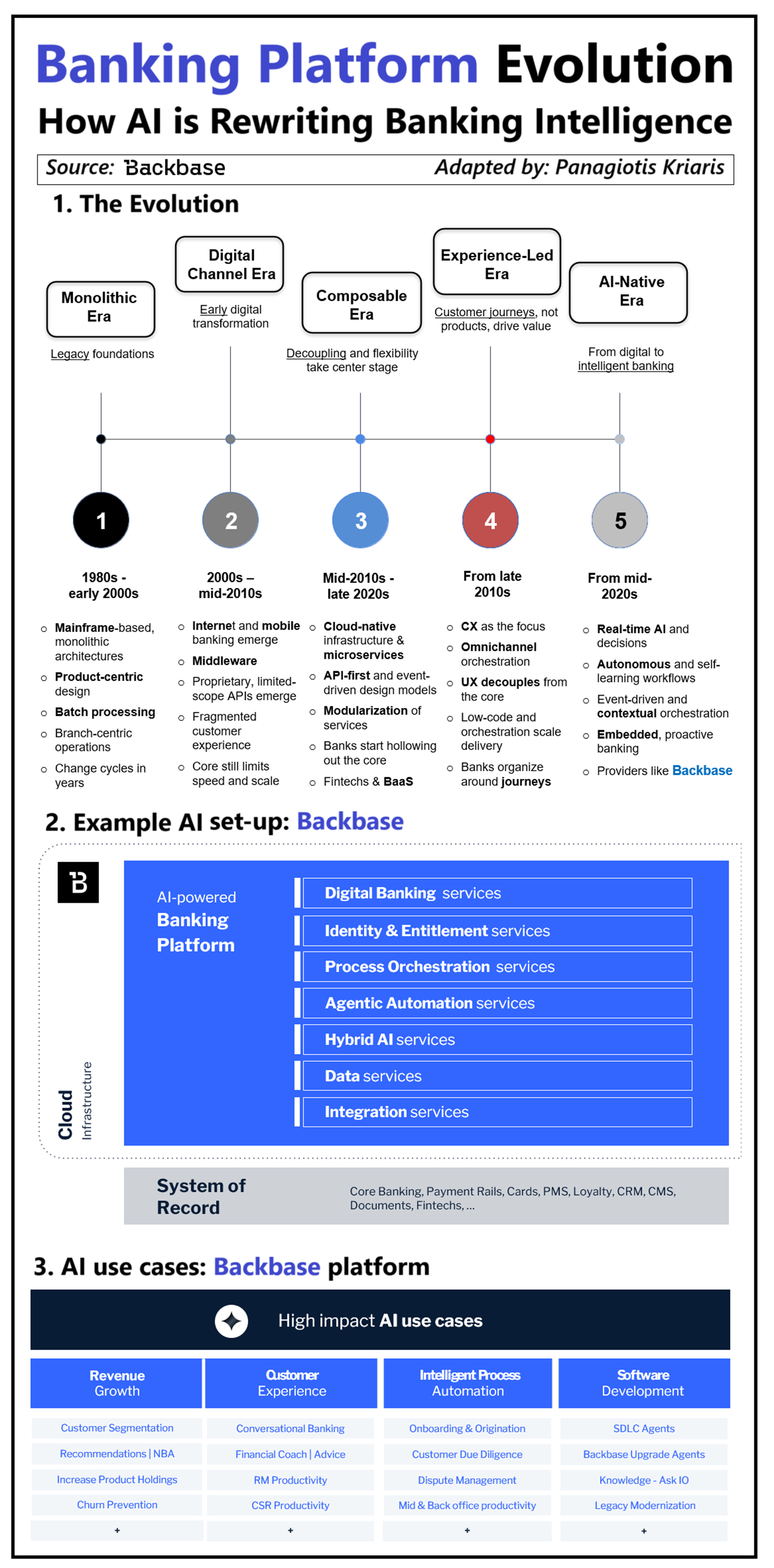

1) Banking Platform Evolution

Banks can’t afford to miss this one. Core banking modernization has long dominated banks’ boardrooms. AI is now flipping the script as it introduces - for the first time in decades - a new operating logic. Here are their options.

For years, core transformation has been treated as a slow, multi-year journey - a balancing act between stability and change. Most banks took a cautious, incremental approach: patch the legacy, layer on digital, expose some APIs, and keep moving. It was less about reinvention - and more about risk containment.

But this time is different.

AI isn’t just another tool to plug into aging infrastructure. It demands - and enables - a fundamentally new way of operating. It runs on real-time data, modular architecture, and continuous orchestration.

Traditional core systems weren’t designed for this. They operate in batch cycles, live in product silos, and require months to adapt to even small changes. Simply adding AI into that environment will not work.

𝗕𝗮𝗻𝗸𝘀 𝗻𝗼𝘄 𝗳𝗮𝗰𝗲 𝘁𝗵𝗿𝗲𝗲 𝗯𝗿𝗼𝗮𝗱 𝗰𝗵𝗼𝗶𝗰𝗲𝘀:

1. Keep modernizing around legacy cores - slow, expensive, and increasingly misaligned with business needs.

2. Attempt a full core replacement - a bold move that requires significant investment and careful execution.

3. Rethink the role of the core entirely - and start decoupling intelligence, orchestration, and engagement from legacy constraints.

That third path is fast gaining traction.

Backbase is one of the leading examples. They’ve recently launched the world’s first AI-powered Banking Platform, built not as a replacement for the core, but as a new operating system around it.

Here’s the set-up:

1. Unified Digital Banking Fabric – orchestrates onboarding, servicing, lending, investing, and more, across all channels.

2. Intelligence Fabric – embeds AI services, agentic automation, predictive models, and responsible AI governance into every layer.

3. Integration Fabric – connects seamlessly to existing cores, CRMs, fintechs, and third-party systems with 60+ pre-built connectors.

4. Composable Architecture – modular, cloud-native, and flexible – banks pick what they need, when they need it, without disruption.

5. Core-Agnostic: It wraps around legacy systems, accelerating transformation without the risks and costs of core replacement.

This isn’t a full core replacement - it’s a strategic rearchitecture. It allows banks to keep what’s stable in the back, while radically upgrading the front and middle with intelligence, flexibility, and speed. It's a modular, composable approach that reflects the reality most banks face: evolve without breaking everything.

AI won’t wait for five-year transformation roadmaps. It’s already reshaping the game - and the banks that win will be the ones building real capabilities, redesigning processes, and deploying at speed.

Opinions: Panagiotis Kriaris, Graphic source: Backbase

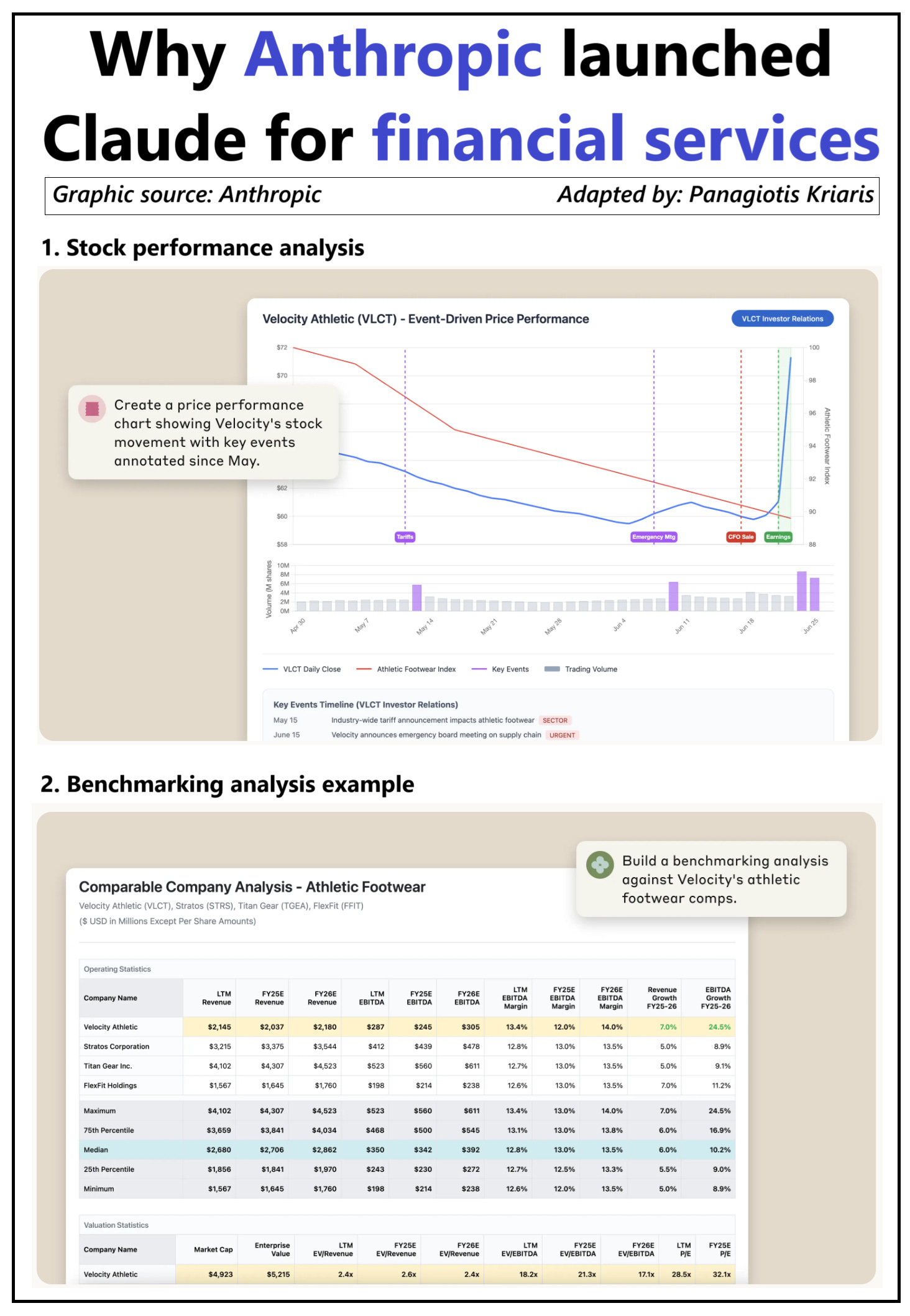

2) Vertical AI models

Domain-specific models are the next chapter in AI’s evolution. Anthropic has delivered one of the first targeted efforts. Why did the pick financial services?

𝗪𝗵𝘆 𝗳𝗶𝗻𝗮𝗻𝗰𝗲?

This is not the first attempt to bring GenAI into the financial sector, but it is one of the first major moves by a foundation model provider to release a tailored product for a regulated industry. Anthropic is betting that general-purpose AI can't meet the demands of regulated, high-risk environments.

Finance is uniquely attractive: it’s a data-rich, document-heavy, regulation-bound industry where speed and accuracy are equally critical. But it's also deeply risk-averse. In tech, speed often comes first. In finance, it’s the opposite - trust, explainability, and control are the most important.

𝗪𝗵𝗮𝘁 𝗽𝗿𝗼𝗯𝗹𝗲𝗺𝘀 𝗱𝗼𝗲𝘀 𝗶𝘁 𝘀𝗼𝗹𝘃𝗲?

It’s less about AI scale, more about AI fit - in finance, the margin for error is very narrow. Claude for FS aims to bridge the gap between capability and deployability. Banks have already experimented with LLMs, but most have hit the same wall: hallucinations, lack of transparency, and outputs that can’t be audited or traced.

By aligning with financial language, processes, and compliance, Anthropic creates a safer path for adoption - enabling AI use in risk, reporting, customer service, and compliance without starting from scratch or inviting regulatory risk.

𝗪𝗵𝗮𝘁’𝘀 𝗻𝗲𝘅𝘁

Anthropic’s move validates what many have already suspected: the future of AI isn’t generalist, it’s vertical. Financial services just happens to be the first industry that demands this level of precision and control. Healthcare, legal, insurance, and government are likely next.

We should expect to see other foundation model players launch their own verticalized offerings soon. And that raises the bar. Off-the-shelf copilots won’t be enough in complex, regulated industries. AI will have to understand the specifics - not just of the language, but of the rules behind it.

𝗜𝗺𝗽𝗹𝗶𝗰𝗮𝘁𝗶𝗼𝗻𝘀

Claude for FS might change the perspective for banks and other FS players trying to build their own ChatGPT-like tools. Until now, many financial institutions have been experimenting with general-purpose models, layering on custom prompts and guardrails. But that’s resource-heavy, risky, and often unsustainable at scale.

Claude for FS offers an off-the-shelf model already tuned to the needs of the industry - language, regulation, and risk included. For many players, it could reset the build-vs-buy question.

Why spend months customizing a generic model when you can start from something already aligned with your context?

Opinions: Panagiotis Kriaris, Graphic source: Anthropic

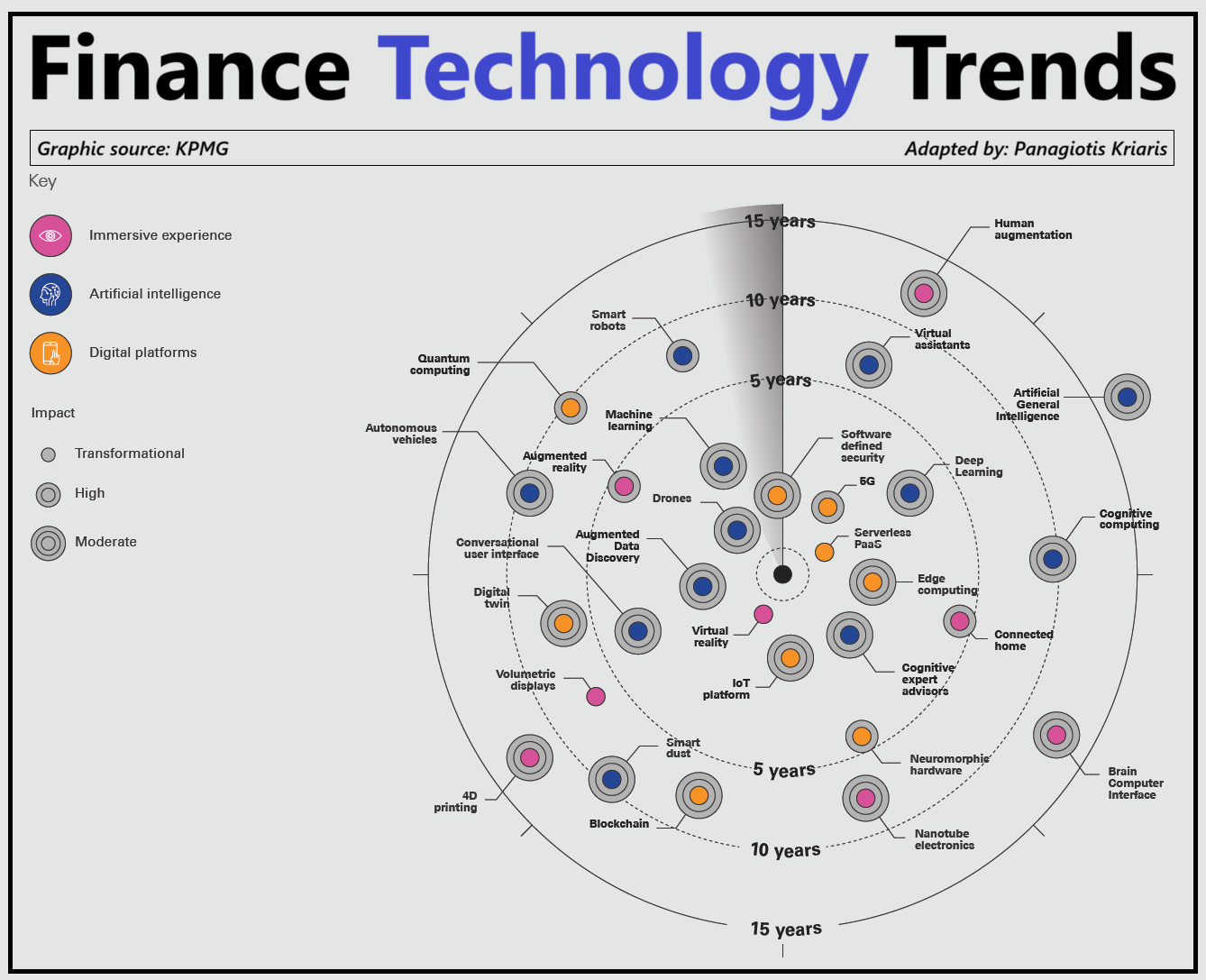

3) Finance Technology Trends

It’s not just about AI. A wave of converging technologies is quietly rewriting the rules of financial services.

𝟭. 𝗔𝗜 𝗿𝗲𝘀𝗵𝗮𝗽𝗶𝗻𝗴 𝘁𝗵𝗲 𝗺𝗶𝗱𝗱𝗹𝗲 𝗼𝗳𝗳𝗶𝗰𝗲

Machine learning and GenAI are starting to handle tasks that used to require expert judgment: risk monitoring, fraud detection, client communication, and even drafting internal reports. With AI agents in the mix, those tasks become continuous and increasingly automated.

Implications: Teams shift from doing the work to supervising it. Accountability now includes both people and systems.

𝟮. 𝗔𝗴𝗲𝗻𝘁𝗶𝗰 𝗔𝗜 + 𝗕𝗹𝗼𝗰𝗸𝗰𝗵𝗮𝗶𝗻

AI agents are moving from tools to actors - able to interpret rules, initiate transactions, and negotiate outcomes. Paired with blockchain’s programmability and auditability, they could create a new execution layer where processes like trade settlement, claims handling, and compliance run end-to-end without human initiation.

Implications: Institutions move from managing processes to governing autonomous systems - with real legal and risk consequences.

𝟯. 𝗜𝗻𝗳𝗿𝗮𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲 𝗮𝘀 𝗮 𝘀𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗽𝗹𝗮𝘆

Edge computing, serverless platforms, and blockchain are removing old bottlenecks. Banks no longer need to build everything themselves - they can plug into modular services and orchestrate ecosystems. That opens the door to faster launches, more partnerships, and entirely new business models.

Implications: Agility becomes a competitive edge. Legacy stacks risk becoming liabilities, no matter the brand strength.

𝟰. 𝗧𝗵𝗲 𝗨𝗫 𝘀𝗵𝗶𝗳𝘁

With the rise of conversational AI, augmented reality, and natural language interfaces, users won’t just tap and scroll. They'll talk, ask, simulate, and explore. These experiences will reshape how people make financial decisions and who they trust to guide them.

Implications: UX becomes a trust driver. How people experience your services will define whether they stick around.

𝟱. 𝗣𝗿𝗼𝗴𝗿𝗮𝗺𝗺𝗮𝗯𝗹𝗲 𝗺𝗼𝗻𝗲𝘆

Attention is shifting from speculative crypto to practical digital money - stablecoins, tokenized deposits, and programmable rails that regulators are beginning to legitimize. They won’t replace traditional finance, but they will build faster, more flexible rails alongside it.

Implications: Banks and central banks must engage with new rails - or risk losing influence over them entirely.

𝟲. 𝗣𝗿𝗲𝗽𝗮𝗿𝗶𝗻𝗴 𝗳𝗼𝗿 𝗾𝘂𝗮𝗻𝘁𝘂𝗺

Quantum computing is a long-term development, but its security risks are already relevant. As the pace of advancement accelerates, safeguarding critical systems today is a necessary investment in future resilience.

Implications: Security strategies will start to shift from defence to preparation.

Opinions: Panagiotis Kriaris, Graphic source: KPMG

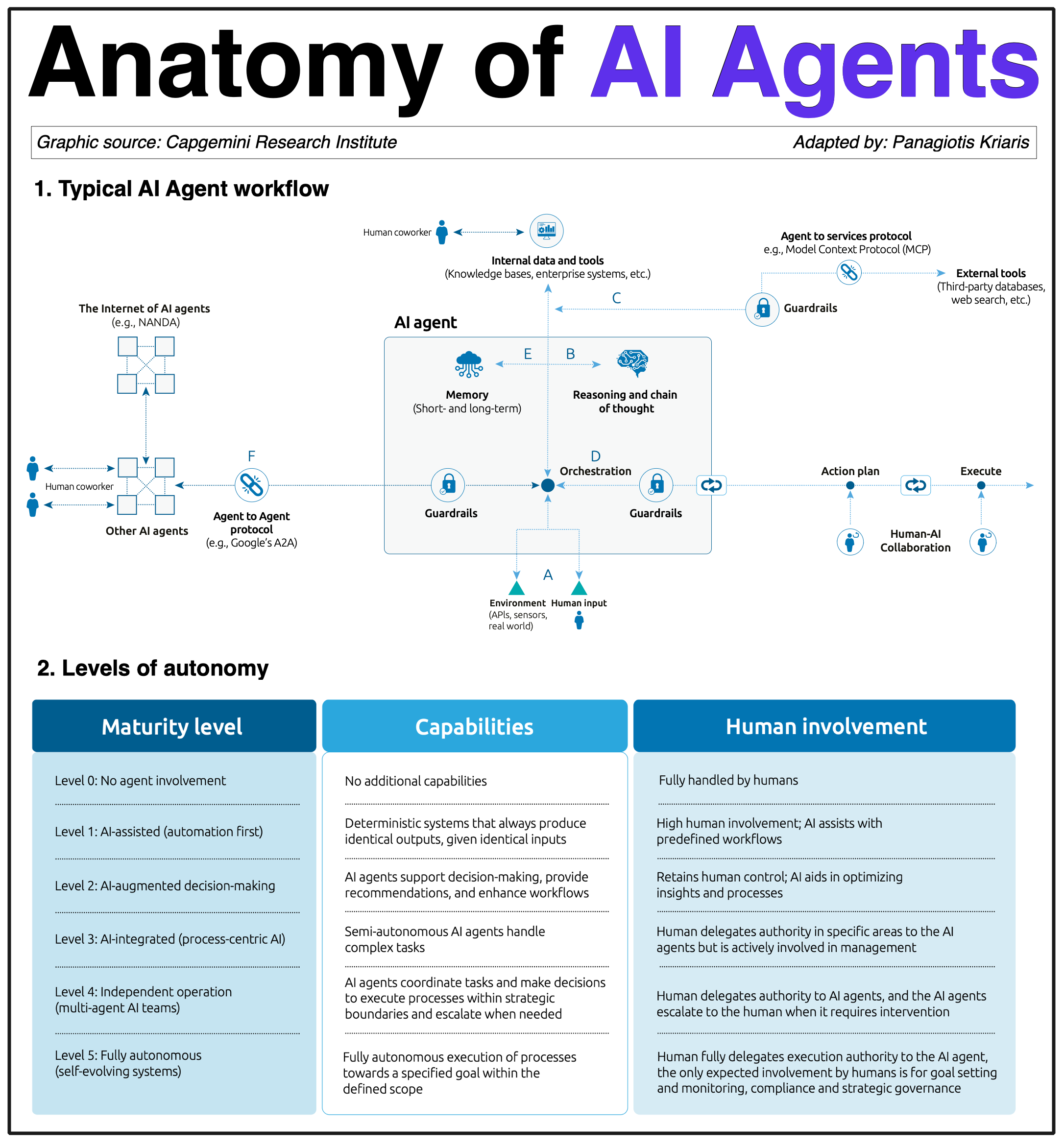

4) Anatomy of AI Agents

AI agents aren’t just the next big thing - they are rewriting the rules of how we think, decide, and execute. Here's how they work.

𝟭.𝗧𝗵𝗲 𝘄𝗼𝗿𝗸𝗳𝗹𝗼𝘄

AI agents operate like autonomous workers. A typical flow includes:

A. Input from the environment: APIs, real-world sensors, or direct human prompts feed raw data into the system.

B. Memory systems: Agents store and recall relevant context — just like a good colleague remembers past meetings or policies.

C. Reasoning engine: They don’t just process — they “think,” applying logic and learned knowledge to make decisions.

D. Orchestration: This is the control room, coordinating multiple steps, tools, or even other agents to complete a task.

E. Guardrails: Built-in rules and policies ensure safe, compliant actions, especially in regulated environments.

F. Agent-to-agent communication: Using emerging protocols agents now talk to one another to complete workflows collaboratively.

𝟮. 𝗘𝘅𝗮𝗺𝗽𝗹𝗲: 𝗦𝗠𝗘 𝗹𝗼𝗮𝗻 𝗮𝗽𝗽𝗿𝗼𝘃𝗮𝗹

Imagine an AI agent working inside a bank’s SME lending unit:

A. A small business applies for a loan. The agent pulls in data from application forms, bank account activity, credit bureaus, and open banking APIs.

B. The agent recalls similar past cases, prior risk models, and policy exceptions. It understands the client’s history with the bank.

C. It evaluates the applicant’s risk profile, compares loan terms, simulates repayment scenarios, and identifies anomalies (e.g., sudden revenue spikes). It flags one item as borderline and prepares justifications.

D. The agent coordinates with other agents specialized in document verification, compliance, credit pricing. Together, they generate a complete credit memo.

E. Built-in rules ensure the loan complies with internal risk limits, ESG criteria, and regulatory obligations. It escalates only if thresholds are exceeded.

F. The agent shares the decision with the treasury and onboarding agents. Treasury adjusts funding allocation; onboarding prepares digital signatures and account disbursement.

What once took weeks and five departments now happens in minutes.

𝟯. 𝗟𝗲𝘃𝗲𝗹𝘀 𝗼𝗳 𝗮𝘂𝘁𝗼𝗻𝗼𝗺𝘆

Not all AI agents are created equal. Capgemini proposes a 5-level maturity scale:

Level 0: No AI. Think manual spreadsheets.

Level 1: AI-assisted workflows. You’re still in charge, AI makes it faster.

Level 2: Augmented decisions. AI provides options, you choose.

Level 3: Integrated agents. They execute within controlled domains.

Level 4: Multi-agent workflows. Like a team of bots handling customer onboarding while another handles compliance.

Level 5: Fully autonomous. Human input shifts to governance and strategy only.

Right now, most companies are stuck at Level 1, but leading firms are already scaling Level 2–3 implementations.

Based on: Capgemini Research Institute / Rise of Agentic AI: https://www.capgemini.com/insights/research-library/ai-agents/

5) Big Banks' Tokenization Bet

This is big news. Tokenization is fast becoming the next battleground for financial infrastructure. Goldman Sachs and BNY Mellon just made one of the boldest moves yet.

Tokenization transforms real-world assets into digital tokens - unique, programmable representations of value that can be transferred, tracked, and embedded into automated financial workflows.

Goldman Sachs and BNY Mellon are turning traditional money-market funds (MMF) into digital tokens. These funds - a $7.1 trillion global market managed by firms like BlackRock, Fidelity, and Federated Hermes - are commonly used by companies and asset managers to hold short-term cash in safe, interest-earning instruments like Treasury bills and commercial paper.

But behind the scenes, they still run on decades-old infrastructure, full of manual steps, cut-off times, and delayed settlements. Tokenization changes that.

𝗛𝗼𝘄?

By bringing the same speed, transparency, and automation we expect from modern payments and applying it to financial instruments that haven’t evolved in decades.

· Instant settlement: Instead of waiting hours (or days) for trades to clear, tokenized assets can settle almost instantly - 24/7, without cut-off times.

· Programmability: Rules and logic (e.g., eligibility checks, compliance constraints) can be embedded directly into the token - reducing manual oversight.

· Fractional ownership: Investors can hold smaller, more flexible portions of a fund, which is hard to do in traditional structures.

· Real-time tracking: Every transfer or ownership change is recorded transparently on a blockchain, improving auditability and risk management.

· Easier collateralization: Tokenized fund shares can be pledged as collateral or moved between counterparties far more efficiently - a big advantage in treasury and liquidity management.

𝗛𝗼𝘄 𝘁𝗵𝗲 𝗽𝗮𝗿𝘁𝗻𝗲𝗿𝘀𝗵𝗶𝗽 𝘄𝗶𝗹𝗹 𝘄𝗼𝗿𝗸:

· BNY Mellon will distribute tokenized money-market funds to institutional clients via LiquidityDirect - its cash management platform that helps treasurers and asset managers invest short-term liquidity.

· Goldman Sachs will record and track ownership of the fund tokens on its private blockchain, providing speed, traceability, and operational efficiency.

· The offering will support tokenized versions of funds managed by major players like BlackRock, Fidelity, and Federated Hermes.

𝗪𝗵𝘆 𝗻𝗼𝘄?

The new U.S. Genius Act gives legal clarity for stablecoins and tokenized assets -removing regulatory uncertainty and unlocking tokenization across mainstream finance.

𝗪𝗵𝗮𝘁’𝘀 𝗻𝗲𝘅𝘁?

This could reshape expectations around liquidity, treasury operations, and how financial assets are managed and settled. Custodians and asset managers will need to adapt. Tokenized Treasuries, equities, and real estate are already being tested.

Opinions: Panagiotis Kriaris, Graphic source: CNBC

Especially great newsletter today! Covering the biggest themes in FS today, with powerful, real-world examples and use-cases.