1) Agentic AI: PayPal vs Mastercard vs Visa 2) AI Agents + Stablecoins vs Subscription Payments 3) Stripe's AI & Stablecoin Play

Welcome to my newsletter! Each week 2-3 hand-picked topics from the world of fintech, payments and banking with behind-the-scenes analysis!

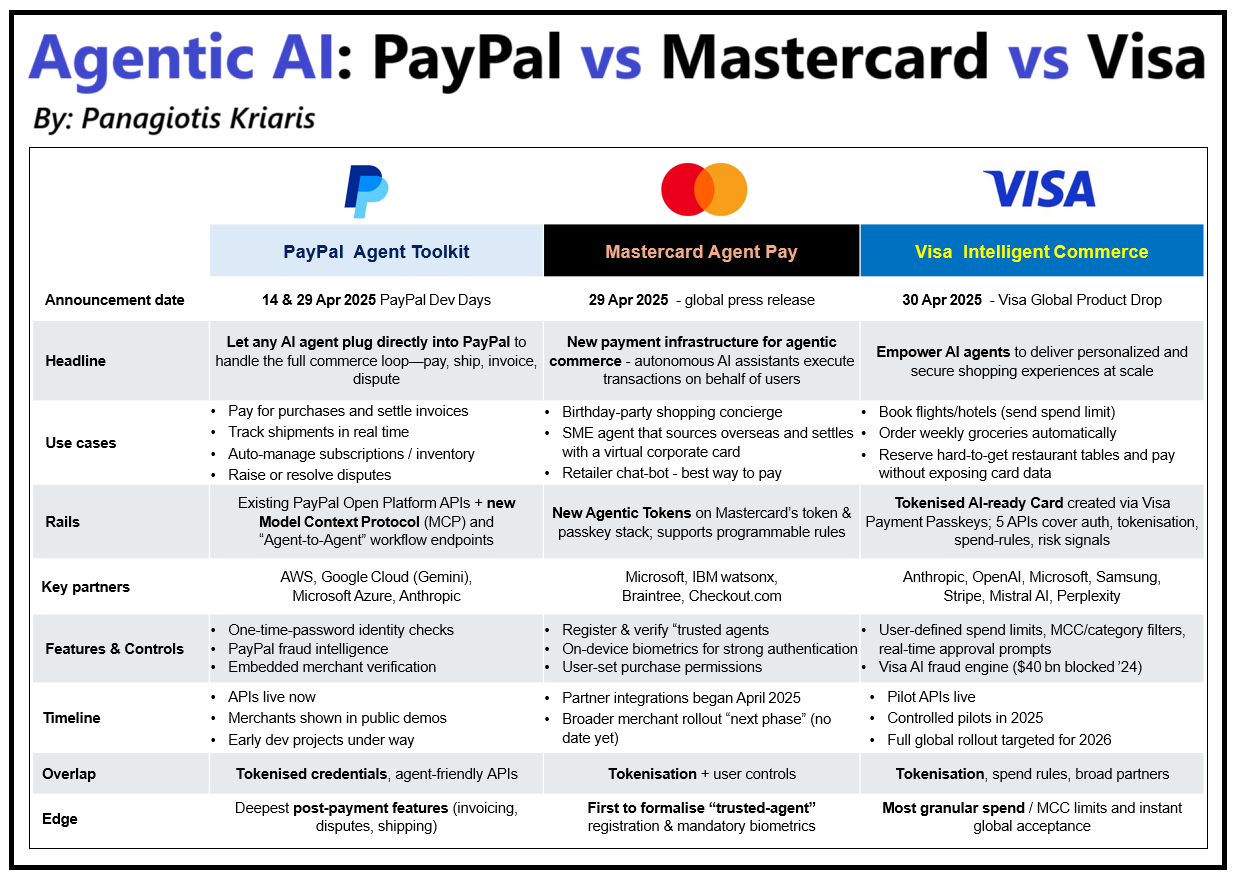

1) Agentic AI: PayPal vs Mastercard vs Visa

The PayPal, Mastercard and Visa announcements are not about agentic AI. They are about ownership of the next chapter of commerce and payments. Here is how they compare.

𝗪𝗵𝗮𝘁 𝗵𝗮𝘀 𝗯𝗲𝗲𝗻 𝗮𝗻𝗻𝗼𝘂𝗻𝗰𝗲𝗱:

- PayPal : APIs that let any AI agent pay, track shipping, issue invoices and resolve disputes without leaving the chat.

- Mastercard : Network tokens + passkeys so agents become “trusted purchasers,” with programmable rules and biometric SCA baked in.

- Visa: Five modular APIs for discovery → checkout, including user‑set spend caps, MCC filters and real‑time approvals.

𝗪𝗵𝗮𝘁 𝗶𝘀 𝗮𝘁 𝘀𝘁𝗮𝗸𝗲?

- The payments race has always been about shaving seconds off checkout. In the agentic era, the winning time is 0 seconds, 0 clicks. Checkout disappears entirely as search, recommendation, and payment collapse into a single LLM-driven conversation.

- Whoever owns the payment credential becomes the default wallet in the loop, capturing not just the transaction, but data, interchange, and value-added services that follow.

- The players that get this right won’t just win conversions. They’ll own the customer relationship. The ones that don’t will find themselves disintermediated by someone else’s agent.

𝗧𝗵𝗲 𝗽𝗼𝘁𝗲𝗻𝘁𝗶𝗮𝗹:

Imagine:

• A travel bot books flights, hotels, insurance and pays - no forms.

• An SME sourcing agent negotiates fabric in Guangzhou and settles with a virtual card - no emails.

• A grocery assistant notices the fridge is low and re‑orders - no conscious decision.

Multiply that by every vertical and every consumer. That’s always‑on demand capture - and potentially trillions in incremental volumes routed through whoever provides the agent‑native rails.

𝗪𝗵𝗮𝘁’𝘀 𝗹𝗶𝗸𝗲𝗹𝘆 𝗻𝗲𝘅𝘁:

1. Industry standards: Common schemas for trusted-agent registration, permissions, and dispute handling.

2. Granular consumer controls: Per-transaction biometrics, spend limits, time-of-day and merchant-category restrictions.

3. Merchant enablement: SDKs and APIs to expose real-time inventory, pricing, and loyalty programs to agents.

4. Regulatory attention: How frameworks like PSD3, CFPB guidelines, or MAS oversight will apply to autonomous payers.

5. New revenue models: Pay-per-call risk scoring, agent onboarding fees, premium fraud protection layers.

6. Advanced risk infrastructure: Real-time monitoring of agent behaviour, intent detection, and adaptive risk scoring to flag anomalies.

7. Liability frameworks: Clear rules for who’s accountable when an agent transacts incorrectly: the user, the platform, or the agent provider.

The race to build the payment infrastructure for autonomous agents is underway. Expect a wave of partnerships, acquisitions, and early execution challenges as the industry adapts to a new model of always-on, agent-driven commerce.

Opinions: my own

2) AI Agents + Stablecoins vs Subscription Payments

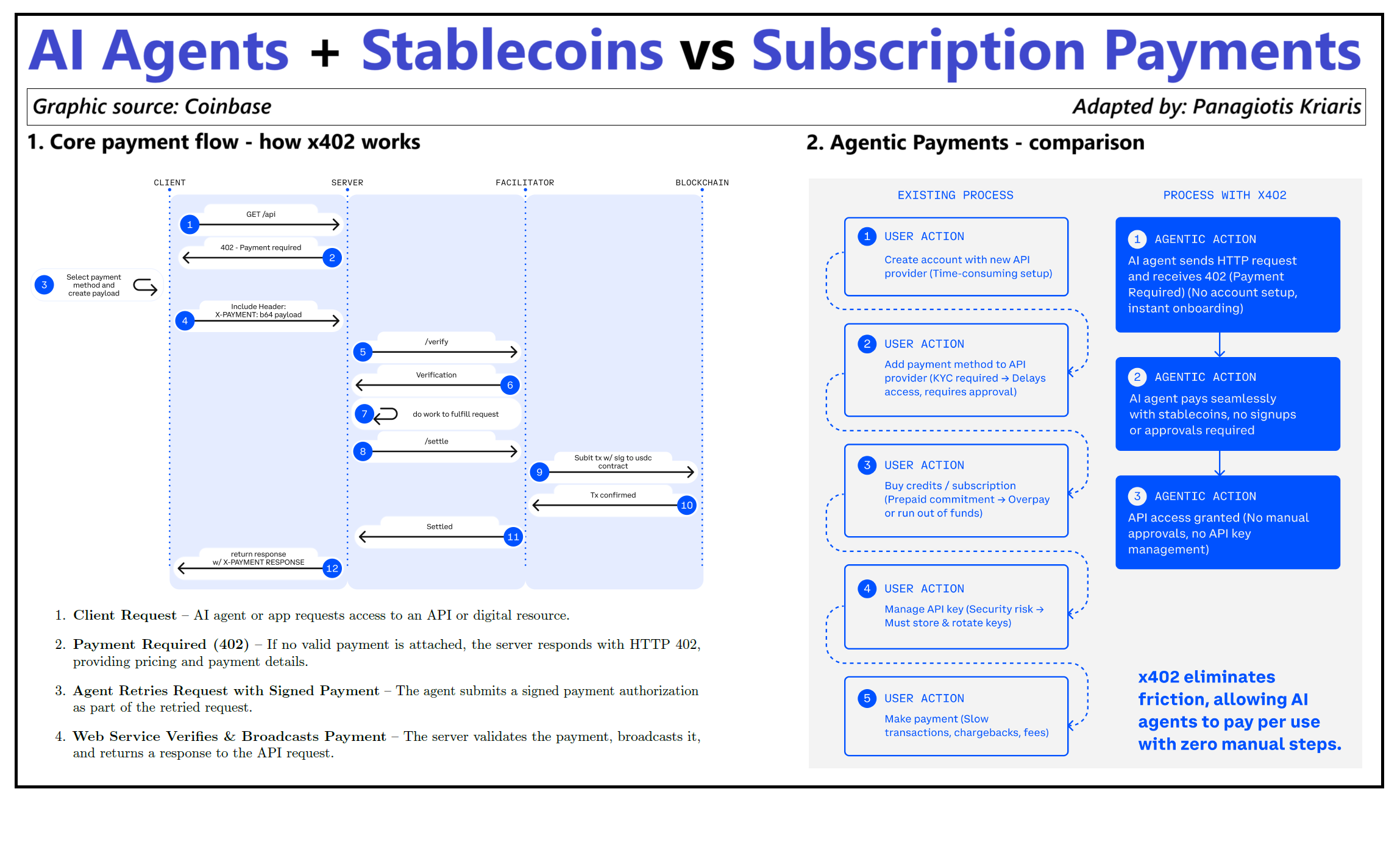

Just announced. AI agents making payments over the internet using stablecoins. Challenging the subscription economy. Is this a game changer? And can it really work? Let's take a look.

𝗪𝗵𝗮𝘁 𝗶𝘀 𝘁𝗵𝗲 𝗽𝗿𝗼𝗯𝗹𝗲𝗺?

While websites can deliver information in milliseconds, paying for that content often requires clunky logins, subscriptions, or credit card transactions. This limits access to small, one-time purchases and forces businesses to rely on ads or subscription models.

𝗪𝗵𝗮𝘁 𝘄𝗮𝘀 𝗮𝗻𝗻𝗼𝘂𝗻𝗰𝗲𝗱?

- x402 is a new open protocol proposed by Coinbase’s developer team. It adds a simple way for websites and applications to request and accept small payments using stablecoins like USDC. Although Coinbase helped launch the idea, x402 is meant to be open-source and available for anyone to use.

- The name comes from HTTP status code 402 Payment Required, which was reserved back in 1992 but never implemented. x402 finally gives it a clear purpose: to allow automated payments over the web using digital money.

𝗛𝗼𝘄 𝗱𝗼𝗲𝘀 𝗶𝘁 𝘄𝗼𝗿𝗸?

1. A person or a bot (AI agent) requests something valuable online (like an article, data, or API service).

2. The server replies with a 402 status and a small price in stablecoins.

3. The user’s wallet (or the AI agent) automatically sends the payment using a blockchain network.

4. Once the payment is received, the server sends the requested content.

In essence x402 wants to make internet payments as easy as getting access to data over the web. Without any need for traditional payment means, tokens or human intervention.

𝗜𝗺𝗽𝗹𝗶𝗰𝗮𝘁𝗶𝗼𝗻𝘀:

- Simple payments: pay for small amounts without subscriptions or accounts.

- AI autonomy: software agents and AI tools making small purchases without human input.

- Global access: anyone with a phone and stablecoin wallet can pay - no bank account needed.

- New business models: websites, APIs, and services can charge per use instead of relying only on ads or subscriptions.

𝗨𝘀𝗲 𝗰𝗮𝘀𝗲𝘀:

- Pay-per-article or video (vs monthly subscription).

- Pay-as-you-go access to weather data, stock prices, etc.

- IoT devices (car or sensor) paying for services (i.e. updates, cloud).

- Pay-per-download for digital products. Musicians, designers, or developers cutting out the platforms.

- In-game purchases without app stores or centralized payment platforms.

- Access to global content and tools without geographical, card, currency or local banking restrictions.

𝗖𝗵𝗮𝗹𝗹𝗲𝗻𝗴𝗲𝘀:

- Adoption: websites and wallets need to support the x402 protocol.

- User experience: simple and secure flows for both people and systems.

- Regulations: stablecoin use varies by country - legal frameworks still developing.

- Security: controls needed against small-ticket transaction fraud.

Opinions: my own, Graphic source: Coinbase

3) Stripe's AI & Stablecoin Play

Two things stand out from Stripe’s announcements last week: AI and stablecoins. And these are real game changers. Far beyond Stripe. Read on to understand why.

Patrick Collison, Stripe cofounder and CEO: “There are not one, but two, gale-force tailwinds, well off the Beaufort scale, dramatically reshaping the economic landscape around us: AI and stablecoins”.

𝗔𝗜 𝗮𝗻𝗻𝗼𝘂𝗻𝗰𝗲𝗺𝗲𝗻𝘁:

- Stripe’s new, large-scale core model - called the Payments Foundation Model - is trained on tens of billions of transactions to capture hundreds of subtle signals about every payment.

- It serves as a single, general-purpose AI backbone that powers and boosts all of Stripe’s specialized payment-focused models (for fraud prevention, authorization optimization, etc.), unlocking performance improvements.

- With its previous models, Stripe gradually reduced card testing by 80% over two years. By applying the new model, Stripe increased its detection rate for attacks on large businesses by 64% practically overnight.

𝗦𝘁𝗮𝗯𝗹𝗲𝗰𝗼𝗶𝗻 𝗮𝗻𝗻𝗼𝘂𝗻𝗰𝗲𝗺𝗲𝗻𝘁:

- Stripe introduced Stablecoin Financial Accounts, its new money-management feature powered by stablecoins, now available to businesses in 101 countries.

- Businesses can hold a balance in stablecoins, receive funds via both crypto (on-chain) and fiat rails (e.g., ACH, SEPA), and send stablecoins almost anywhere in the world.

- For now only two US dollar–pegged coins are supported: USDC and Bridge’s USDB.

𝗦𝘁𝗮𝗯𝗹𝗲𝗰𝗼𝗶𝗻 𝗰𝗮𝗿𝗱:

- To enable merchants that only accept fiat, Stripe’s newly acquired Bridge partnered with Visa to issue cards that automatically convert stablecoins to local currency at the point of sale - usable at any of Visa’s 150 million+ merchants worldwide.

- This isn’t minting a new stablecoin token; it’s issuing a Visa-branded payment card that draws on a customer’s Stripe stablecoin balance.

- The card automatically converts USDC or USDB into local fiat at the point of sale.

𝗜𝗺𝗽𝗹𝗶𝗰𝗮𝘁𝗶𝗼𝗻𝘀:

By unifying payments intelligence into one foundation model and pairing it with native stablecoin rails, Stripe is laying the groundwork for a radically leaner, more resilient financial plumbing:

- transactions can be dynamically routed through the optimal network in real time based on risk, cost, and speed assessments from a single AI brain;

- authorization decisions become instantly adaptive to emerging fraud patterns;

- settlement shifts from multi-day, multi-party reconciliations to near-instant, atomic on-chain transfers.

This convergence not only slashes friction and latency at every step but also collapses traditional silos - acquiring banks, card networks, correspondent banks - into programmable, API-driven flows, fundamentally redefining how money moves, who controls it, and how securely it can be managed.

Opinions: my own, Graphic source: Stripe