1) 2024 FinTech Review 2) How Banks can monetize Open Banking

Happy New Year and welcome to my newsletter! Each week two hand-picked topics from the world of fintech, payments and banking with behind-the-scenes analysis!

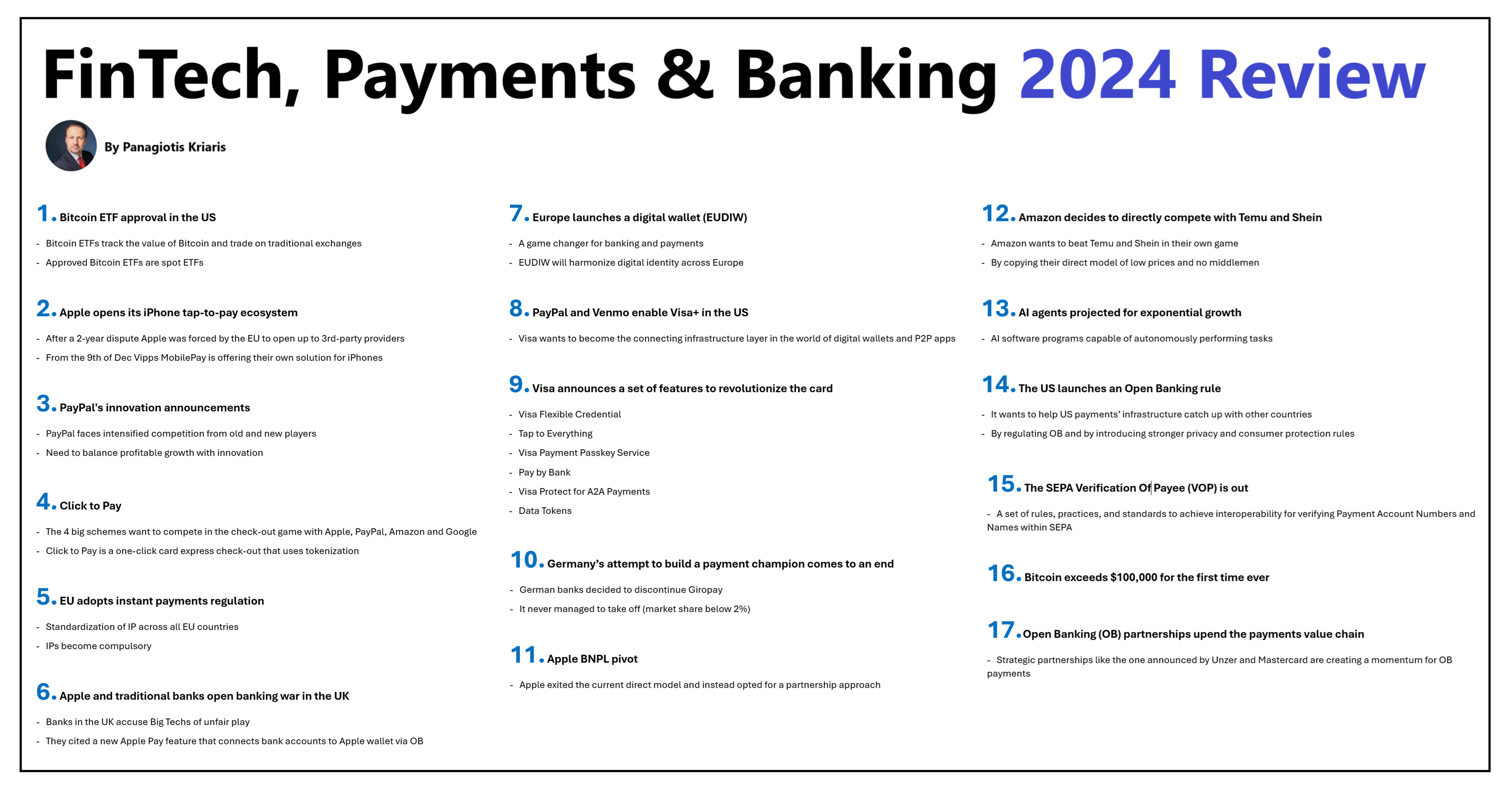

1) 2024 FinTech Review

2024 is over and this is my shortlist of events that shaped the world of fintech, payments and banking in 2024.

1. Bitcoin ETF approval in the US

- Bitcoin ETFs track the value of Bitcoin and trade on traditional exchanges

- Approved Bitcoin ETFs are spot ETFs

2. Apple opens up its iPhone tap-to-pay ecosystem

- After a 2-year dispute Apple was forced by the EU to open up to 3rd-party providers

- From the 9th of Dec Vipps MobilePay is offering their own solution for iPhones

3. PayPal's innovation announcements

- PayPal faces intensified competition from old and new players and needs to balance profitable growth with innovation

4. Click2Pay

- The 4 big schemes want to compete in the check-out game with Apple, PayPal, Amazon and Google via a one-click card express check-out that uses tokenization

5. EU adopts instant payments regulation

- Standardization of IP across all EU countries

- IPs become compulsory

6. Apple and traditional banks open banking war in the UK

- Banks in the UK accuse Big Techs of unfair play citing a new Apple Pay feature that connects bank accounts to Apple wallet via OB

7. Europe launches a digital wallet (EUDIW)

- A game changer for banking and payments

- EUDIW will harmonize digital identity across Europe

8. PayPal and Venmo enable Visa+ in the US

- Visa wants to become the connecting infrastructure layer in the world of digital wallets and P2P apps

9. Visa announces a set of features to revolutionize the card:

- Visa Flexible Credential

- Tap to Everything

- Visa Payment Passkey Service

- Pay by Bank

- Visa Protect for A2A Payments

- Data Tokens

10. Germany’s attempt to build a payment champion comes to an end

- German banks decided to discontinue Giropay after it never managed to take off (market share below 2%)

11. Apple BNPL pivot:

- Apple exited the current direct model and instead opted for a partnership approach

12. Amazon decides to directly compete with Temu and Shein

- Amazon wants to beat Temu and Shein in their own game by copying their direct model of low prices and no middlemen

13. AI agents projected for exponential growth

- AI software programs capable of autonomously performing tasks based on broadly defined, open-ended goals

14. The US launches an Open Banking rule

- It wants to help US payments’ infrastructure catch up with other countries by regulating OB and by introducing stronger privacy and consumer protection rules

15. The SEPA Verification Of Payee (VOP) is out

- A set of rules, practices, and standards to achieve interoperability for verifying Payment Account Numbers and Names within SEPA

16. Bitcoin exceeds $100,000 for the first time ever

17.Open Banking (OB) partnerships upend the payments value chain

- Strategic partnerships like the one announced by Unzer and Mastercard are creating a momentum for OB payments

2) How Banks can monetize Open Banking

Despite a common perception to the contrary, open banking is one of the (incumbents) banks’ best bets to go on the offensive and find new monetization opportunities. Let’s take a look.

It’s true that open banking has created for banks new compliance requirements that are eating up resources and attention. What is sometimes not realized though, is that at the same time it opens up a much-needed window of opportunity in a world that is moving at break-neck speed:

— Data and APIs are now the building blocks of the new economic model, in which innovation is customer rather than product-driven

— Banks that are not able to properly connect and consume data via APIs, are essentially banned from the innovation that is happening

— The traditional banking model of vertically integrating static products in a closed-loop set-up is no longer a viable option

— The fiercest competition is no longer coming from the inside of the industry but rather from adjacent segments or even from the outside

Adapting to this reality is a one-way street for banks. Here’s how:

— As a starting point, banks need to change their vertically integrated and product-focused approach to an open set-up that is built on integrating third-party and fintech offerings via APIs

— Despite clearly falling outside their comfort zone, the opportunity for banks lies in combining existing elements like trust and customer positioning with new ones like technology and data analytics

— As the ecosystem becomes more advanced and adapts to customer needs, it will become increasingly difficult for banks to go it alone with nothing more than their own apps

— As long as they keep their customers happy, banks do not necessarily have to own everything they offer

A recent paper from Whitesight, AFS + Brankas has summarized well banks’ monetization opportunities across 4 clusters:

1) Banks work with external developers and incentivize them to use their premium APIs to create innovative solutions while generating revenue from API subscriptions and usage.

2) Banks monetize their license and infrastructure by offering BaaS APIs and services to fintechs, merchants and other third parties.

3) Banks position themselves as intermediaries, offering a platform for third-party fintechs and developers. These marketplace and platform APIs encompass lead generation, product catalog management, partner relationship tools, and recommendation engines. Banks profit by facilitating valuable interactions between fintechs and customers.

4) Banks leverage open banking APIs themselves to build value-added services that improve the customer experience and generate additional revenue streams.

The more successful banks manage to perform in this strategy, the higher up they can move in the new value chain and subsequently the more new revenue sources they can generate.

Opinions: my own, Graphic sources and monetization opportunities: Whitesight, AFS + Brankas (Link to the Whitesight and Brankas report: https://resources.brankas.com/future-of-financial-services-trust-mena-region)